- Jay Parsons' Rental Housing Economics

- Posts

- Round 3 of REIT Earnings Calls: AMH + 3 More Apartment REITs

Round 3 of REIT Earnings Calls: AMH + 3 More Apartment REITs

Four more REITs: American Homes 4 Rent, BSR REIT, Elme Communities, Clipper Realty

Jay Parsons

August 09, 2024

Sponsored by: Madera Residential

This is Part 3 (and grand finale) of highlights from REIT earnings call season. Today, we’ll round up four REITs, starting with on the SFR side with American Homes 4 Rent, followed by three apartment REITs: BSR REIT, Elme Communities, Clipper Realty.

If you missed the first two editions of REIT reports, you can find links at the bottom of this newsletter to both.

As always, this commentary is not investment advice (nor should it be interpreted as such) — just stuff I found interesting.

American Homes 4 Rent (AMH)

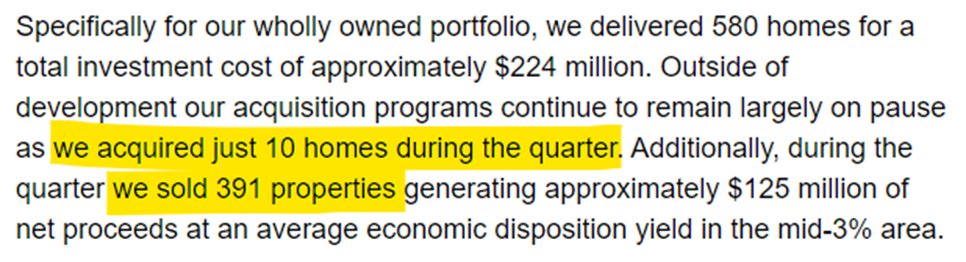

1) AMH was a net seller in Q2-- buying only 10 houses, while selling 391. (But it is developing a bunch, too.)

As a research nerd, one of my pet peeves is seeing headlines and policy chatter that focus only only ACQUISITIONS, not DISPOSITIONS. It’s net flows that matter. AMH was a net seller in Q2 even as its expanded over time. (More broadly: the SFR sector overall has actually seen contraction due to mom-and-pop exits and individual homebuyers outbidding investors from 2016-2023.)

- Chris Lau, AMH

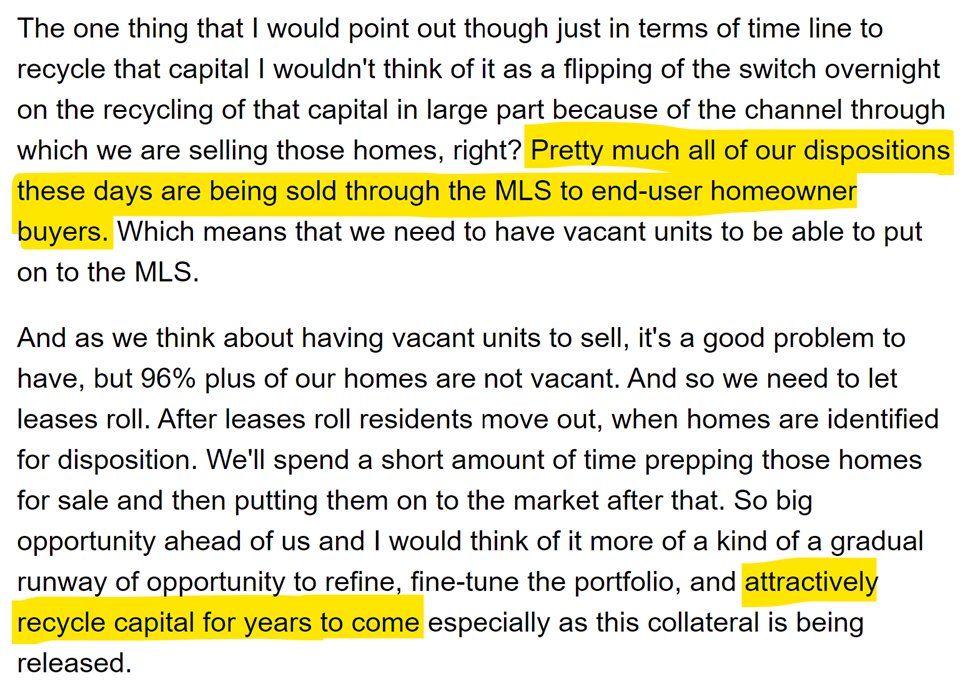

2) More dispositions could be coming. AMH offered some great color on their disposition process. When AMH sells homes, the buyer is usually an individual homebuyer. AMH generally only sells houses after a renter moves out -- and it sounds like they could look to sell more as move-outs occur.

- Chris Lau, AMH

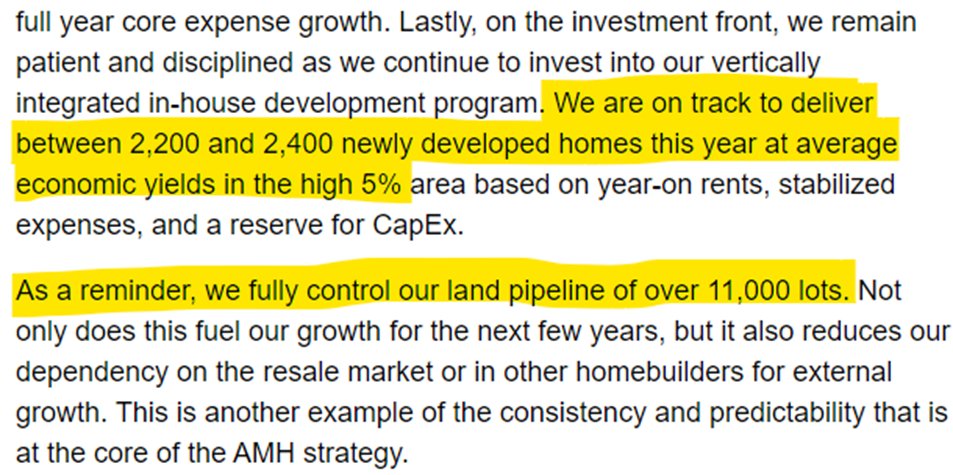

3) AMH has put a lot of focus on building new housing, and it expects to complete between 2,200-2,400 new single-family rental homes in 2024. Additionally, AMH owns another 11k lots and looking to buy more land. Bullish on new development.

Both AMH and Invitation Homes have pivoted in recent years to prioritize being creators of new housing — albeit through different strategies. Personally, I think we’ll see more and more of this going forward given a) more efficient operations of BTR versus scattered site SFR, b) more efficient capital deployment, c) stiff competition for buying individual homes, and d) regulatory pressure intensifying around institutional investors buying houses — even though misguided.

- Bryan Smith, AMH

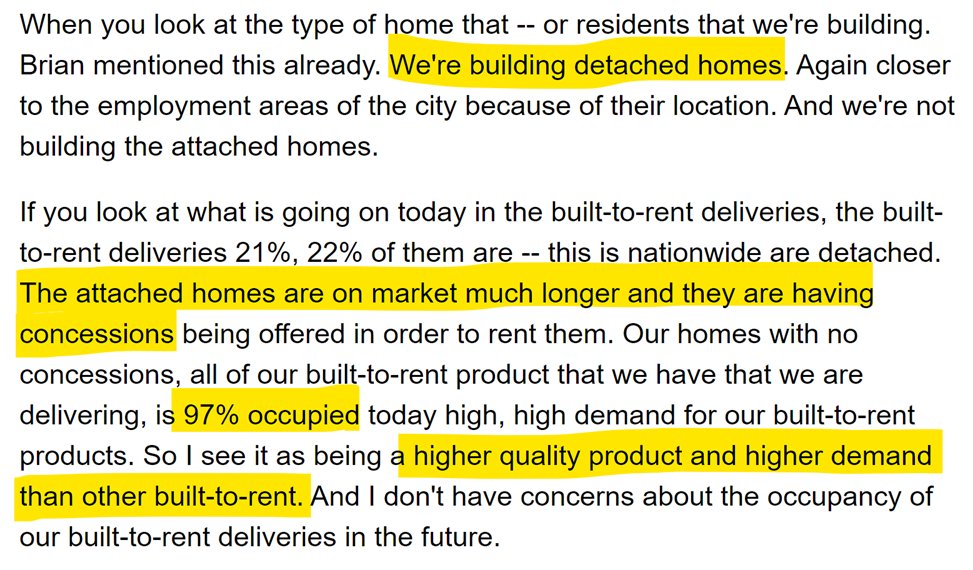

4) AMH sees detached BTR performing stronger than attached BTR. Asked about supply competition in the BTR (build-to-rent) space, AMH noted its building a scarcer product-- detached single-family rental homes, where occupancy rates remain very high even in high-supplied markets like Phoenix.

This view also aligns with reporting from John Burns Research & Consulting, which shows softer performance among “horizontal apartments” (kind of a hybrid apartment/BTR format) and townhomes than in detached single-family rental homes.

- David Singelyn, AMH

5) On rents, AMH reported rent growth topping 5% for both new leases and renewals. One stat the highlights the stark differences between lesser-supplied SFR versus higher-supplied multifamily: AMH reported new lease rents outpacing renewals.

By comparison, most apartment REITs reported negative new lease rents combined with solid growth in renewal rents — which has compressed loss-to-lease (gap between new lease rents and in-place rents).

- Bryan Smith, AMH

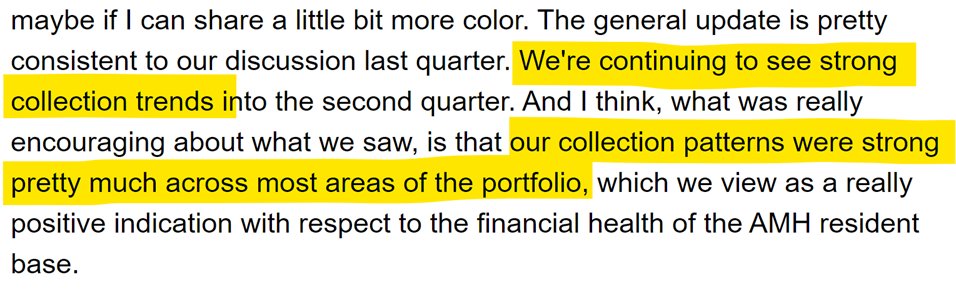

6) At the same time, AMH reported bad debt down to 90 bps -- which means the vast majority of renters are paying the rent each month. AMH said "collection patterns were strong pretty much across most areas of our portfolio." This aligns with reporting across the entire REIT sector (apartments and SFR) showing renters in increasingly strong financial shape with rising incomes, high retention and low delinquency.

- Chris Lau, AMH

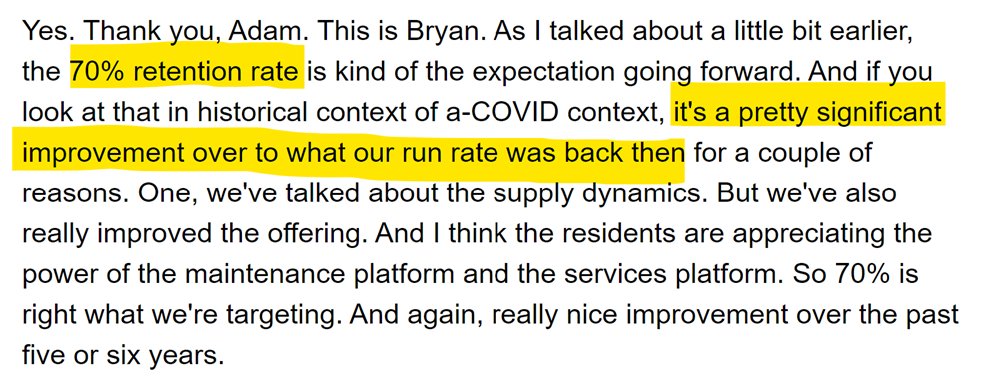

7) Retention rates remain high -- and AMH expects more of the same going forward.

- Bryan Smith, AMH

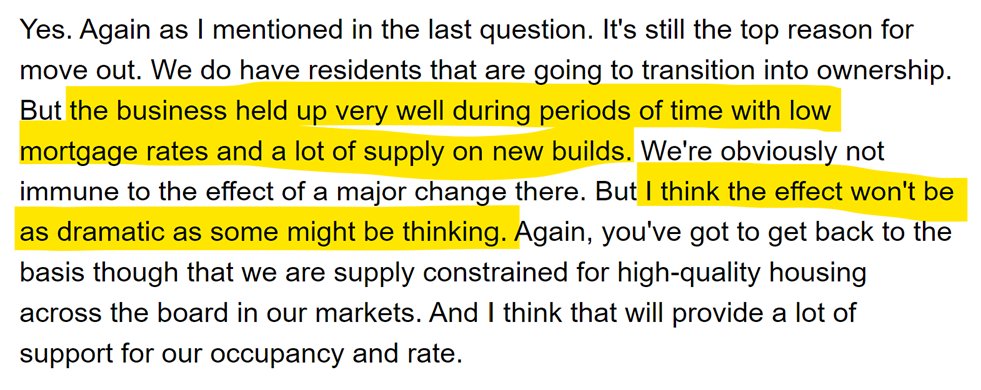

8) AMH downplayed the impact of a potential drop in mortgage rates. Analysts asked about the potential impact to single-family rental demand if mortgage rates drop back down and boost homebuying. AMH (very rightly) noted the rental housing sector performed very well even when rates were low and homebuyer demand was strong.

This is one of those persistent myths that just doesn’t go away because the myth intuitively makes sense even if there’s no historical data to support it. Generally speaking, for-sale housing demand and for-rent housing demand move together. A rising tide boosts all ships.

- Bryan Smith, AMH

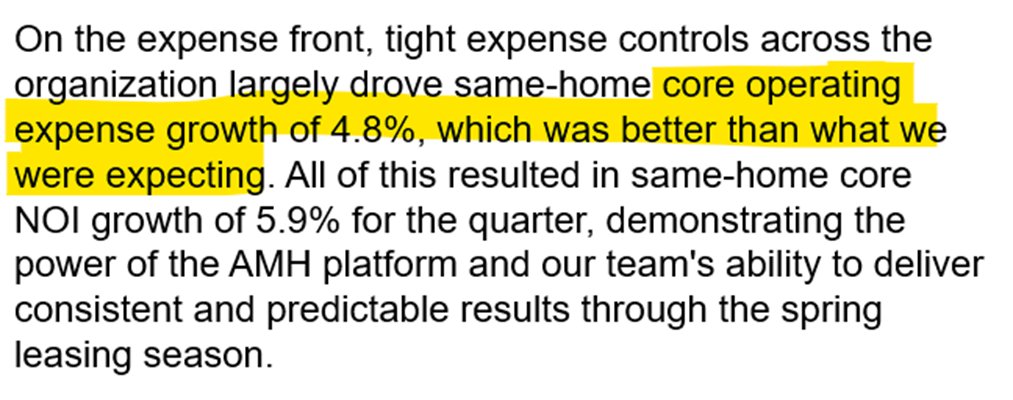

9) On expenses, AMH reported expense growth came in below expectations -- and also reduced guidance on future expense growth, too. AMH credited "mostly favorable" property tax trends and its operational efficiency efforts.

- Bryan Smith, AMH

10) AMH also noted improvements in property insurance premiums. This has been a major theme for apartment operators, but we've seen more mixed news for SFR of late -- so it's a positive sign that AMH sees progress.

- Chris Lau, AMH

11) Looking at individual markets, AMH called out the Midwest region and the Carolinas as top performers.

- Bryan Smith, AMH

12) AMH reported strong in-migration into their Midwest markets, while also noting their properties in the Midwest tend to feature large yards. (The Midwest has been a strength for apartment investors, too, but only a couple apartment REITs have much presence there.)

- Bryan Smith, AMH

BSR REIT (BSR)

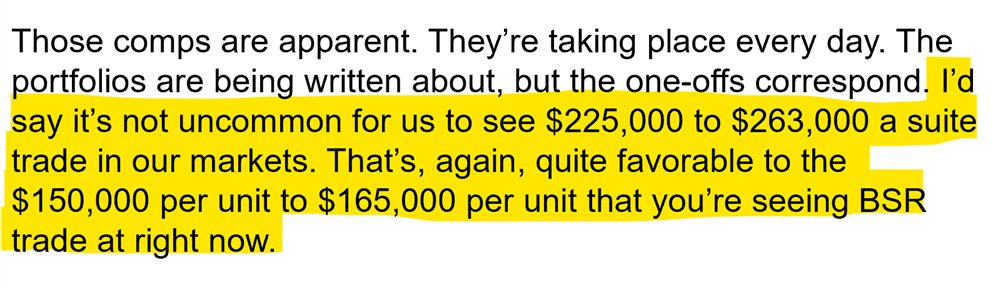

1) Like most apartment REITs, BSR noted the wide disconnect between where properties are trading versus how REITs are valued. Asked about EQR's $1b acquisition, BSR did some quick math comparing the price per unit versus BSR’s implied value.

- Dan Oberste, BSR

2) Like its peers, BSR appears to be increasingly bullish on finding acquisition opportunities again as the market starts to find its footing. (Note that BSR is concentrated today in Texas, Oklahoma and Arkansas.)

- Dan Oberste, BSR

3) BSR, like everyone else, is feeling the impact of peak supply in Texas -- keeping new lease rents negative. But on the positive side, BSR also noted that demand "has exceeded our expectations," especially in Dallas.

- Dan Oberste, BSR

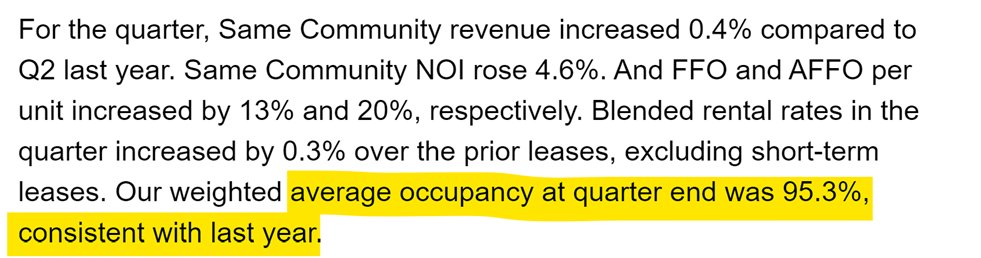

4) Strong demand helped keep occupancy flat year-over-year in spite of new supply competition at 50-year highs, though it clearly did impact rents. Occupancy in the 95-96% range for multifamily is generally considered “essentially full” when accounting for normal churn.

- Dan Oberste, BSR

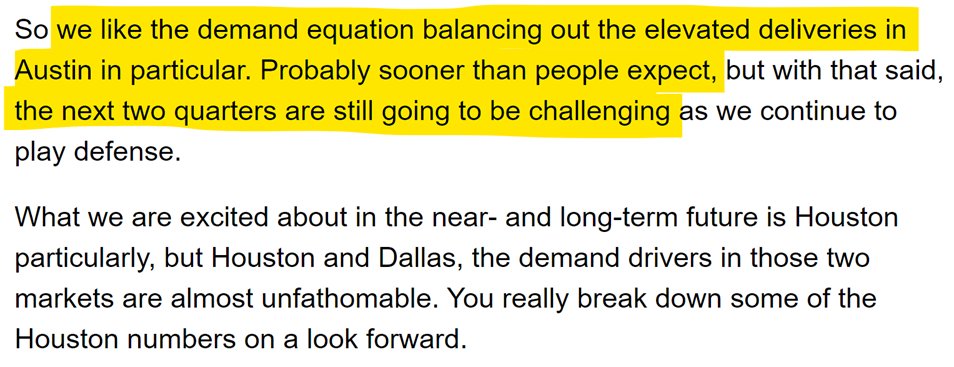

5) BSR is seeing signs of life in Austin. Many apartment operators have singled out Austin as a particularly challenged market given ultra-high supply (even if still strong demand, just not enough to keep pace). BSR sees the same, but thinks the recovery could be "sooner than people expect."

Also called the demand drivers in Dallas and Houston “almost unfathomable,” assuming they remain intact as supply drops considerably. (And also worth noting Houston has built much less, on a size-adjusted basis, than its peer markets like Dallas.)

- Dan Oberste, BSR

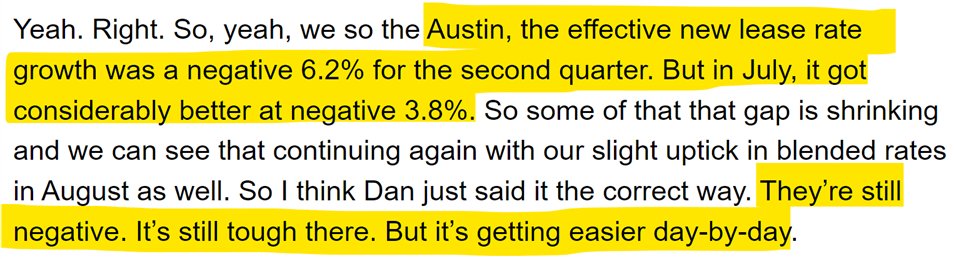

6) One reason for BSR's optimism: Rent cuts are moderating in their Austin portfolio. Rents are still falling, but not as much as they were previously. "They're still negative ... but it's getting easier day-by-day."

- Susie Rosenbaum, BSR

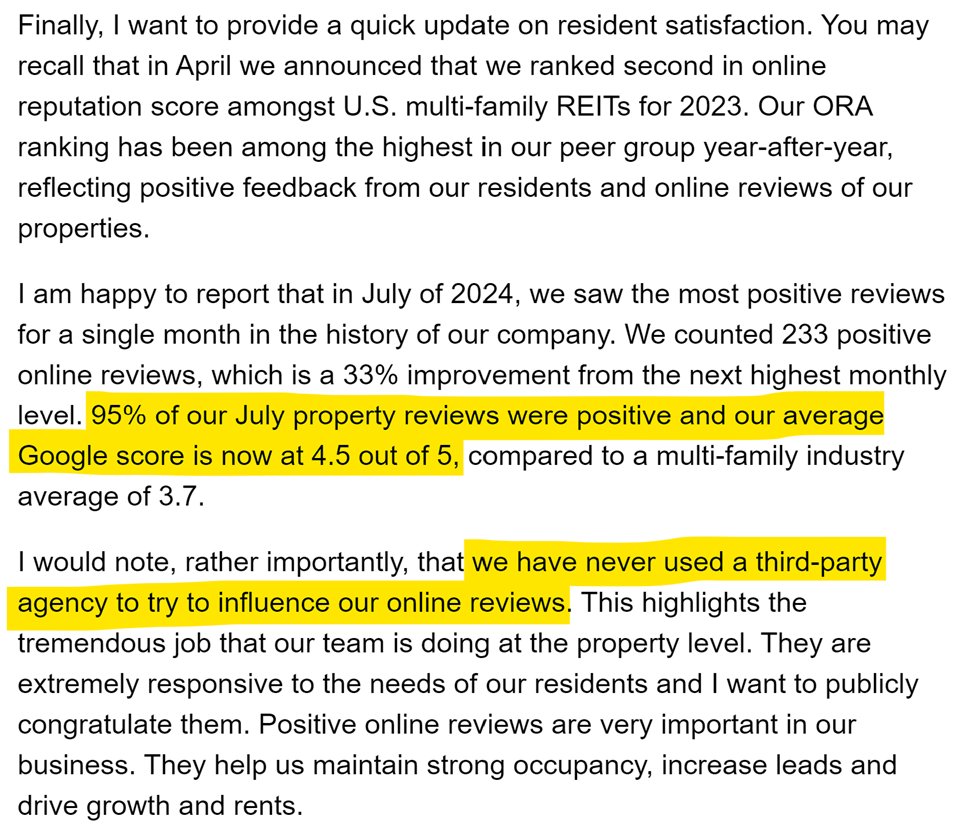

7) On operations, BSR had some interesting commentary and data on resident satisfaction and online reviews... and credited its reputation scores for boosting leasing traffic and occupancy. (Note: ORA = Online Reputation Assessment.)

- Dan Oberste, BSR

8) On expenses: Like many of its peers, BSR reported that property insurance premiums (which had been skyrocketing in prior years) are now more favorable.

- Susie Rosenbaum, BSR

Elme Communities (ELME)

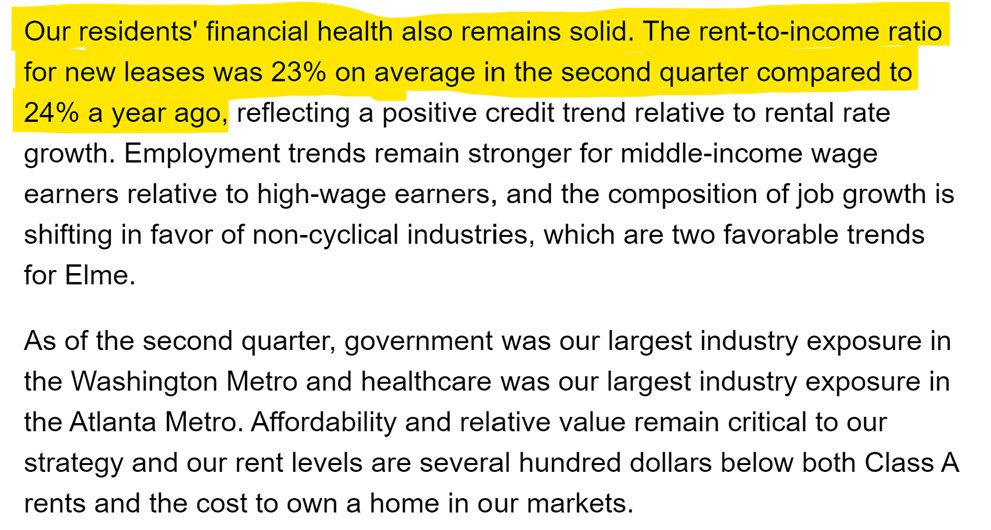

1) Elme (which is mostly middle-market Class B, concentrated in metro DC area and in Atlanta metro) sees strong financial health among renters, with rent-to-income ratios inching down to 23%.

- Paul McDermott, Elme

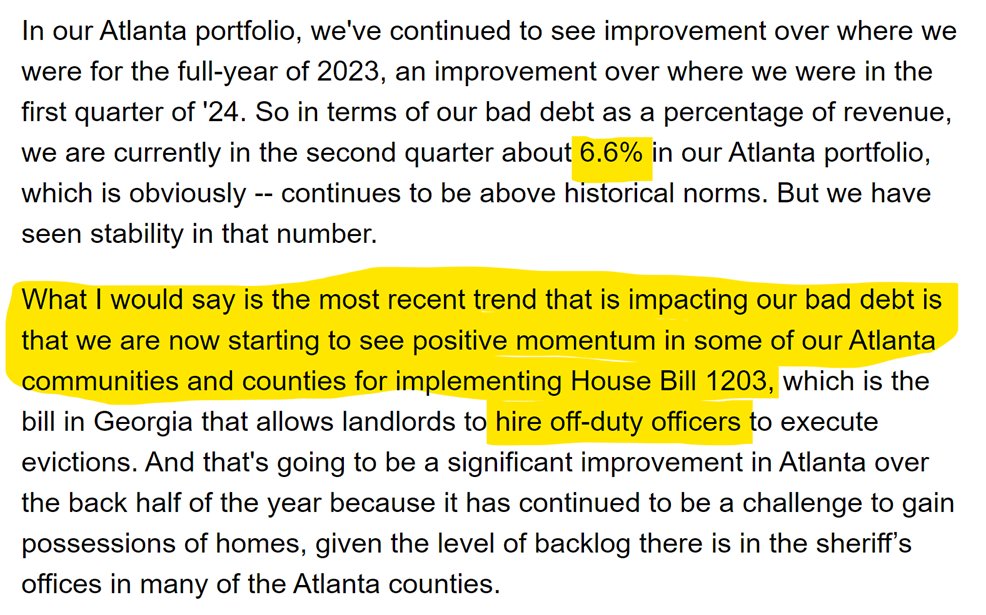

2) But Elme says it continues to wrestle with challenges from pandemic-era leasing fraud in Atlanta combined with very slow-moving courts, keeping bad debt relatively high. Elme did credit a new state law for pushing some improvement.

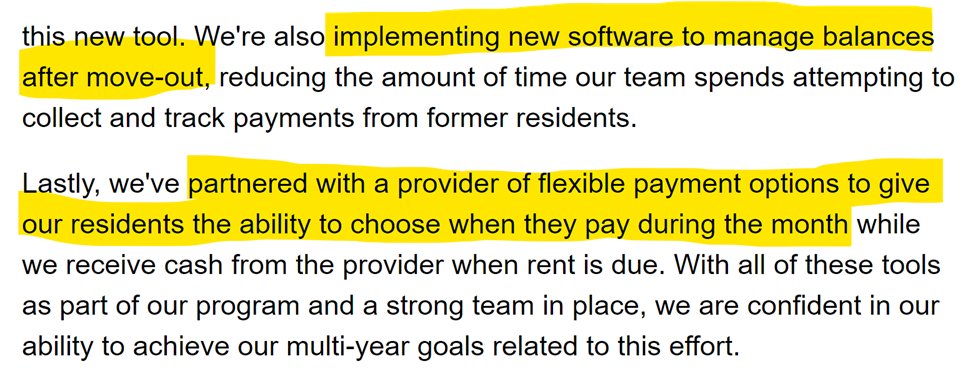

- Tiffany Butcher, Elme

3) Elme highlighted a few tech initiatives to combat those trends, including a) reducing leasing fraud at the front end, b) offering flexible payment options to renters struggling to pay rent on time every month, and c) managing balances after move-out.

- Tiffany Butcher, Elme

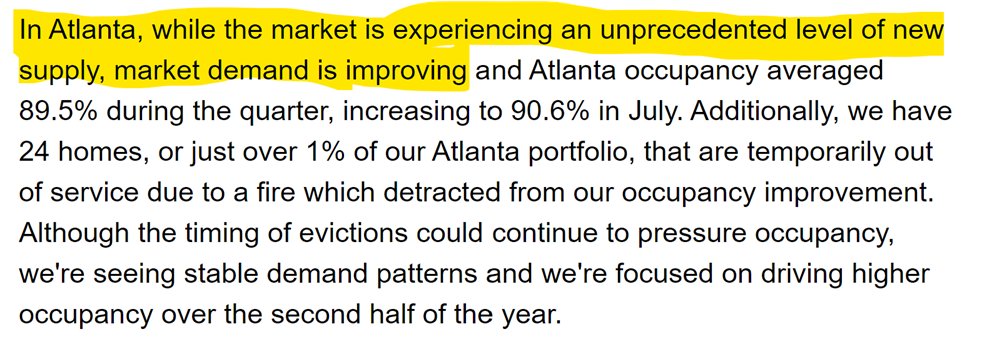

4) Atlanta has been a tough market for most apartment operators (not just Elme) due to leasing fraud. (NMHC survey showed it was top market for fraud) combined with elevated new supply hitting that market. Still soft fundamentals, but Elme did report upward momentum in July, with occupancy moving upward.

- Tiffany Butcher, Elme

5) Going north to DC (where Elme has had much longer-term presence dating back to its days as Wash REIT), it's a much different story of stronger performance. "The demand patterns that we're seeing in Northern Virginia ... are exceptional."

- Tiffany Butcher, Elme

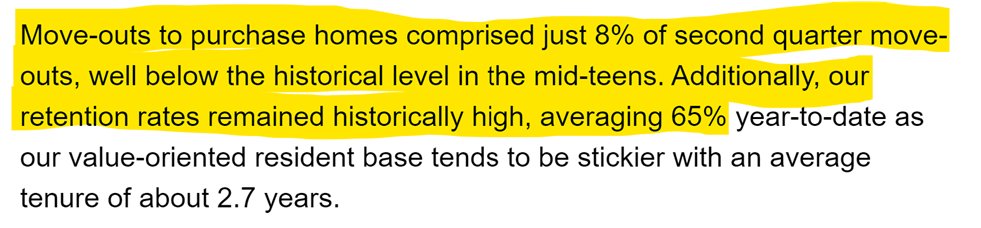

6) Like others, Elme reported very high retention rates and very low move-outs to home purchase. Retention came in at 65% year-to-date, which is quite high even compared to today’s elevated market norms.

- Paul McDermott, Elme

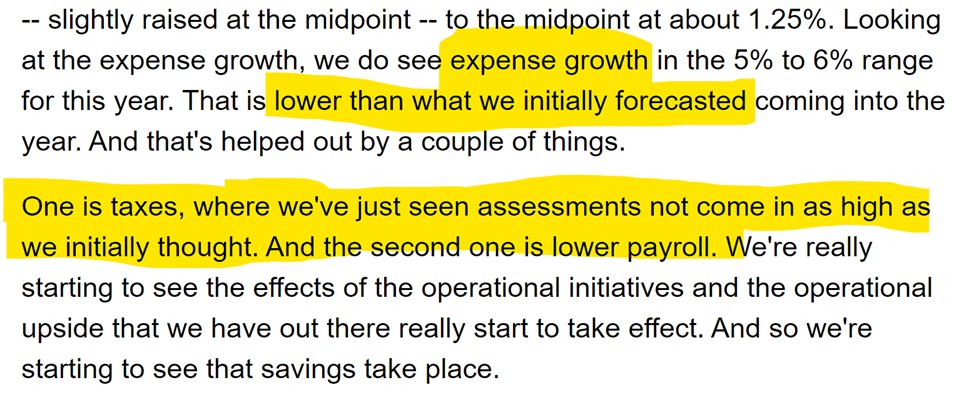

7) Also like others, Elme is seeing moderation is expenses and reduced its outlook on expense growth for the year. Property taxes came in below projections, and Elme also credited new "operational initiatives" in controlling payroll growth.

- Paul McDermott, Elme

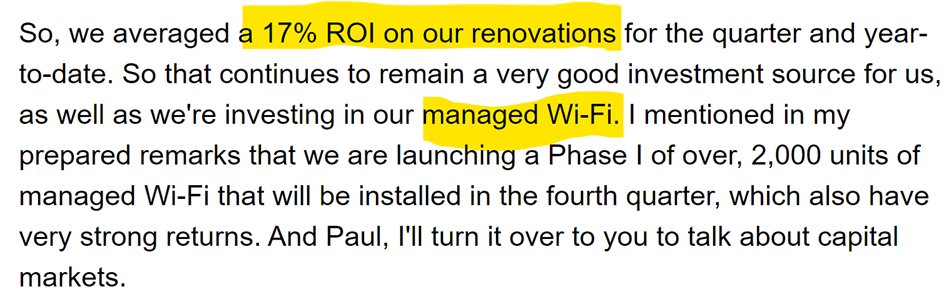

8) Also like others, Elme reported some solid numbers on ROI from renovations despite the high-supply environment. Elme also talked about managed Wi-Fi, which is usually a win/win deal where renters get high-speed WiFi at better price and operator gets some ancillary revenue.

- Tiffany Butcher, Elme

Clipper Realty (CLPR)

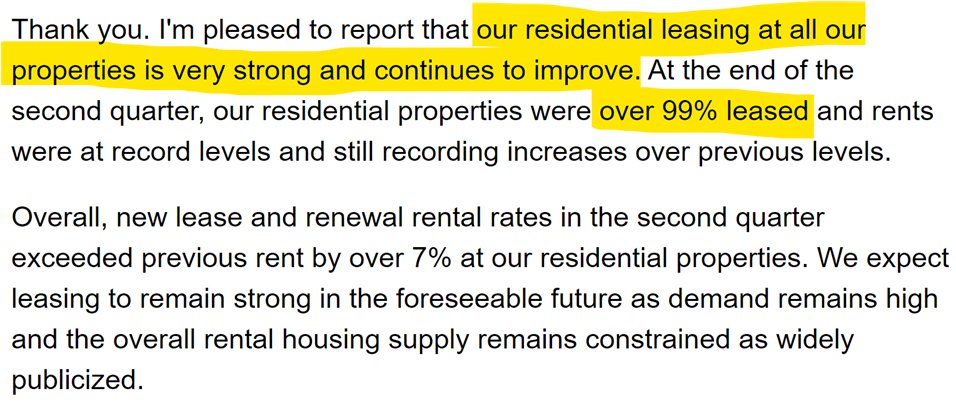

1) Leasing demand is "very strong and continues to improve," and >99% leased with rents up >7% thanks to New York City’s "constrained" supply. Note that Clipper is a small apartment REIT operating only in the New York City area, so its commentary is isolated to that market.

- JJ Bistricer, Clipper Realty

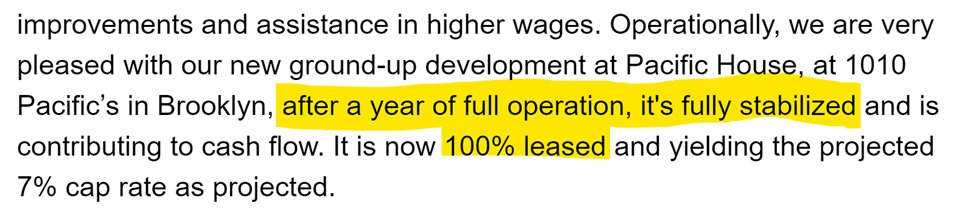

2) Clipper built a new apartment development that reached 100% occupancy "after a year of operation." If that's defined by start of leasing, it's a brisk lease-up pace that developers in most other cities aren't experiencing these days given volume of supply competition. But as they noted earlier, New York City is its own universe.

- David Bistricer, Clipper Realty

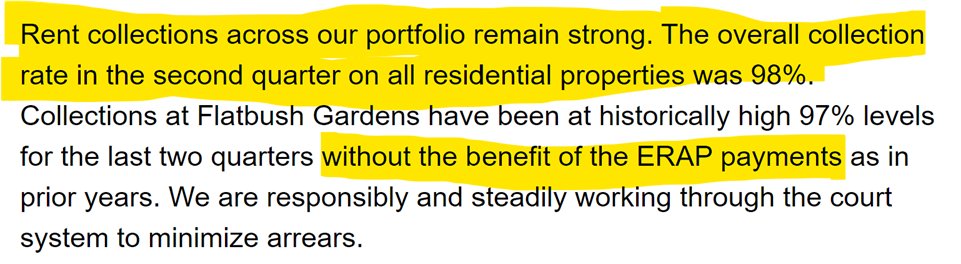

3) Perhaps more surprising than the first two items: Rent collections reached 98% even "without the benefit of ERAP (federal rental assistance) payments," which I'd assume is higher than NYC market averages.

- JJ Bistricer, Clipper Realty

Wrapping Up REIT Earnings Season:

In case you missed the first two newsletters, here’s where you can find them:

Round 1: Invitation Homes, Equity Residential, Centerspace, NexPoint Residential, Veris Residential.

Round 2: MAA, AvalonBay, Essex, UDR, Camden, Independence Realty Trust (IRT).

Additionally, I posted a high-level recap of the multifamily REITs collective updated on LinkedIn this week. You can find that here. I’ll post a similar update on SFR soon.

As a reminder once again: None of what I write about REITs (or otherwise) is intended to be investment advice whatsoever, nor is it a comprehensive look at any REIT. I just write about the things I find interesting.

Thank you to the sponsor of this newsletter, Madera Residential. Click the image above to learn more about Madera’s multifamily platform.