- Jay Parsons' Rental Housing Economics

- Posts

- Round 2 of REIT Earnings Calls: 5 Big Apartment REITs

Round 2 of REIT Earnings Calls: 5 Big Apartment REITs

Five multifamily REITs talking shop: MAA, AvalonBay, Essex, UDR, Camden, IRT

Jay Parsons

August 05, 2024

Sponsored by: Madera Residential

This is Part 2 of highlights from REIT earnings call season. Today, we’ll round up six more large multifamily REITs: MAA, AvalonBay, Essex, UDR, Camden, Independence Realty Trust (IRT). And then we’ll follow up later this week with more.

Last week, we hit the highlights from the first five: Invitation Homes, Equity Residential, Centerspace, NexPoint Residential and Veris Residential. You can find that post here if you missed it.

As always, this commentary is not investment advice (nor should it be interpreted as such) — just stuff I found interesting.

Mid-America Apartment Communities (MAA)

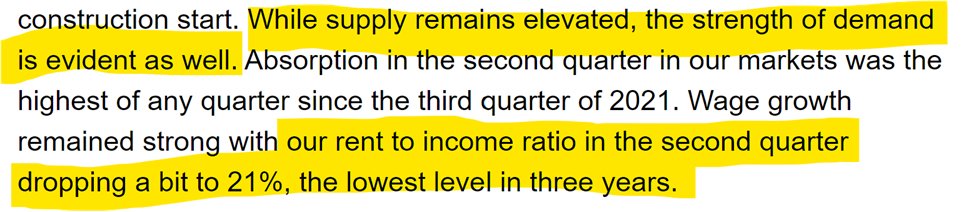

1) Strong affordability tailwinds pushing rent-to-income ratios down to 21%. The average renter household income came in at $91k, compared to $75k at the start of 2020. MAA (like others) is also seeing strong demand for apartments at today’s rent levels.

- Tim Argo, MAA

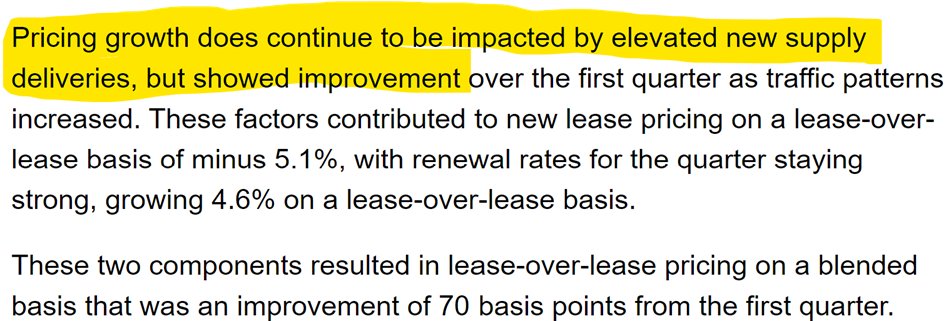

2) But of course, there's even more supply than demand -- especially in the Sun Belt. Supply levels are at record highs (or at least multi-decade highs) nearly everywhere. So new lease rents are falling more for MAA and other Sun Belt REITs than for coastal REITs — even as renewal rents prove pretty resilient.

- Tim Argo, MAA

3) MAA singled out Austin, Atlanta and Jacksonville as three markets with the most supply-driven challenges. New lease rents down 8-9% in metro Atlanta, with Midtown noted as "our worst concessionary environment right now, sometimes pushing 3 months" free rent.

- Tim Argo, MAA

4) Some Sun Belt markets remain in better shape, especially mid-sized markets — including even some high-supplied tertiary/secondary markets like Charleston and Savannah.

- Tim Argo, MAA

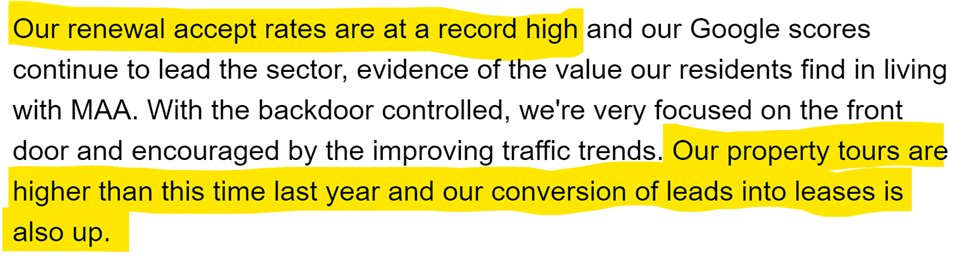

5) But even with all that supply, it's a positive surprise (to me anyway) to see renewal acceptance rates are at a "record high," which mirrors unexpectedly low turnover across the industry. Strong retention came even with MAA's renewal rent growth at +4.6%. You’d think with all this supply out there, we’d see more renters moving out to chase better deals, and while some of that does exist, it’s not happening at scale you might expect.

- Brad Hill, MAA

6) Like others, MAA is seeing record low move-outs to purchase (with just 12.4% of move-outs coming due to home purchase) — which explains some of the high retention, but clearly isn’t the only factor.

- Tim Argo, MAA

7) Renters are paying rent each month, with “net delinquency representing just 0.3% of billed rents” — which is quite low, and one category where the Sun Belt is still outperforming most coastal cities.

- Tim Argo, MAA

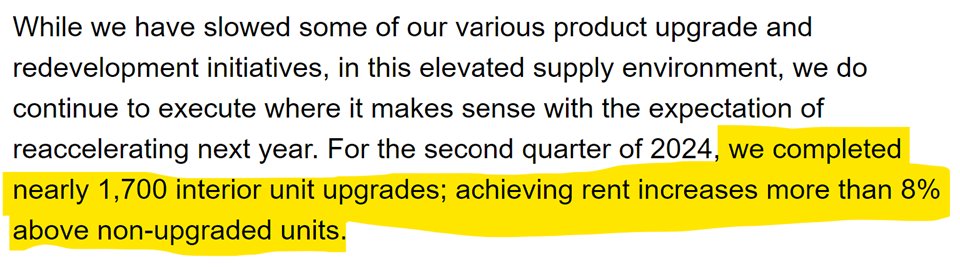

8) MAA is still achieving solid ROI on renovations/value-adds, as some other REITs reported as well. This is another semi-surprise just because the challenge with value-add in a high-supply environment is that renters may be able to find newer apartments for similar price-- so it's a tough balance.

- Tim Argo, MAA

9) While new lease rents remain down, MAA reported improved momentum directionally, and projected YoY asking rent growth would rebound to positive territory in August -- something that hasn't happened in 18 months. If that sticks, it might be significant inflection point.

- Eric Bolton, MAA

10) One thing to watch: Loss-to-lease (gap between new lease rents & in-place rents), now at 2%. Generally speaking, compressing loss-to-lease usually means less renewal rent upside, since asking rents are very transparent online and your residents can make easy comparisons.

If new lease rents do indeed pick back up, that would help retain solid renewal rent growth and avoid an undesirable "gain to lease" scenario.

- Tim Argo, MAA

11) MAA joined the chorus of voices reporting expense growth > rent growth while at the same time seeing moderation in expense growth, lowering guidance on expenses. MAA reported favorable trends in expenses for repairs and maintenance, property taxes and payroll, while noting it expected to see most controllable expenses “continue to run at a pretty normal rate.”

- Clay Holder, MAA

12) MAA appears bullish on both acquisitions and new construction -- especially given the massive drop in new starts, pointing to an improved outlook on fundamentals.

- Eric Bolton, MAA

13) Like others, MAA sees cap rates settling around 5% (subtly taking a dig at Wall Street's higher cap rate assumptions / lower NAVs). MAA highlighted a recent acquisition of the variety everyone loves right now-- Sun Belt new construction priced well below replacement cost.

- Brad Hill, MAA

14) Lots of interesting talk about development, with MAA appearing to position itself to stay somewhat active amidst a period where it's really tough to start new projects. Started two projects in Q2, with another 11 projects in pre-development.

- Brad Hill, MAA

15) MAA eluded to a strategy to acquire fully entitled (shovel ready) projects from other developers who are unable to secure the financing needed to break ground. It’s an intriguing concept and something other REITs talked about on their calls, too.

- Brad Hill, MAA

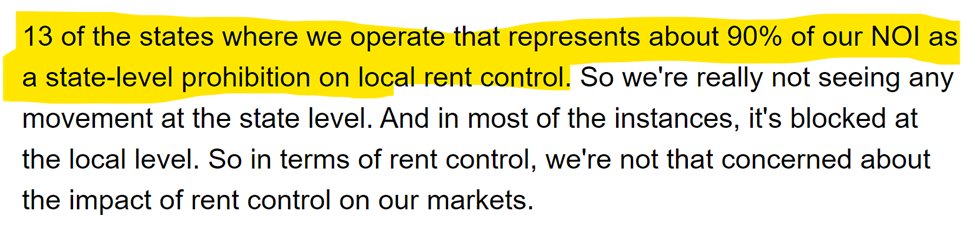

16) Asked about rent control possibilities, MAA downplayed concerns about federal legislation and highlighted its geographic footprint. MAA noted it's primarily operating in markets with statewide bans on rent control.

High-supplied markets tend to be places without rent controls, not coincidentally.

Rob DelPriore, MAA

AvalonBay Communities (AVB)

1) AvalonBay (the nation’s 2nd-largest apartment REIT with >90k units) reported strong resident retention, high occupancy, solid rents ... but sticky challenges with small number of long-term nonpayers.

- Benjamin Schall, AvalonBay

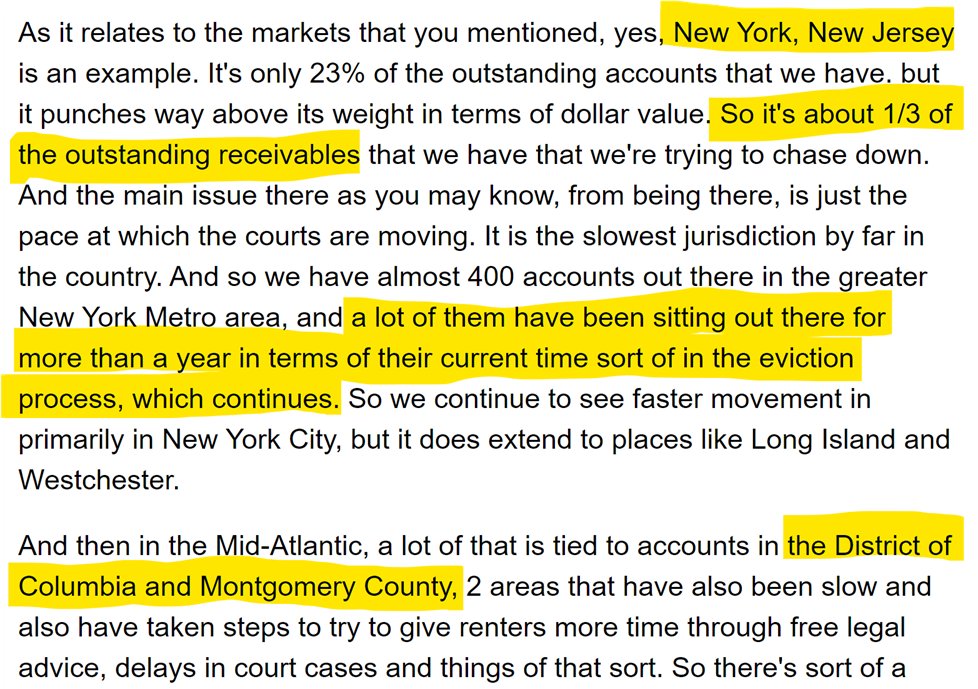

2) Bad debt (unpaid balances) expected to be at 1.7% for 2024 (down 60 bps YoY), but still 2-3x above pre-COVID norm, and materially higher than non-coastal REITs -- largely due to challenges in New York area.

- Sean Breslin, AvalonBay

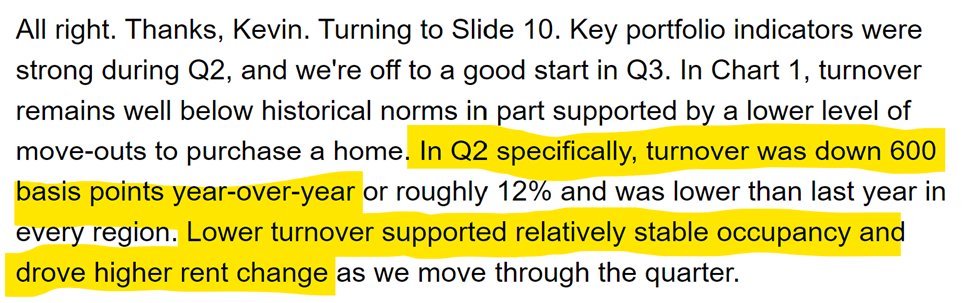

3) Like other REITs, AVB is seeing above-normal resident retention rates this year, with turnover down 600 bps year-over-year

- Sean Breslin, AvalonBay

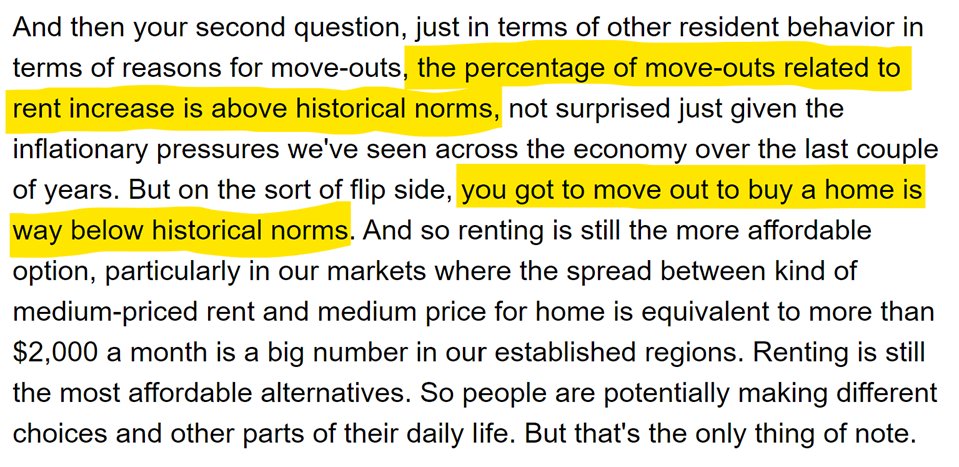

4) Like others, AVB is seeing retention boosted by very low move-outs to home purchase. Unlike others, though, AVB (which generally is high-end Class A / coastal suburban) said it's seeing move-outs due to rent increases slightly elevated.

- Sean Breslin, AvalonBay

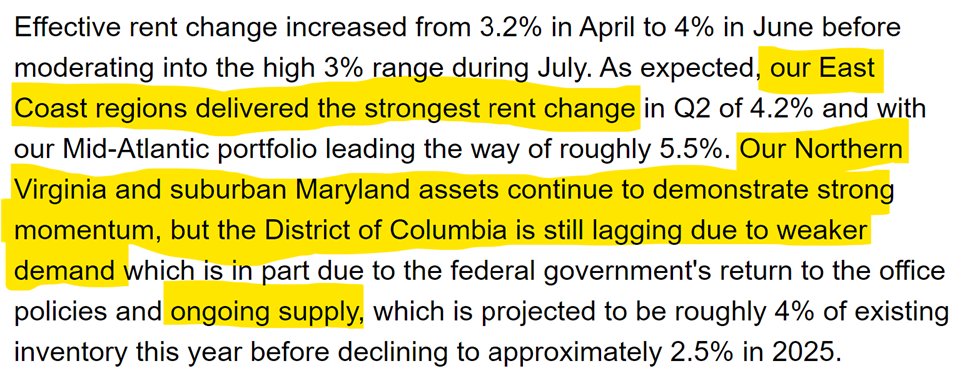

5) Low-supplied coastal suburbs (AVB's sweet spot) has been top-performing niche nationally for rents, boosting AVB. Like EQR and UDR, AVB singled out the East Coast as top-performing region -- and specifically highlighted suburban DC ... while noting softness in the District.

- Sean Breslin, AvalonBay

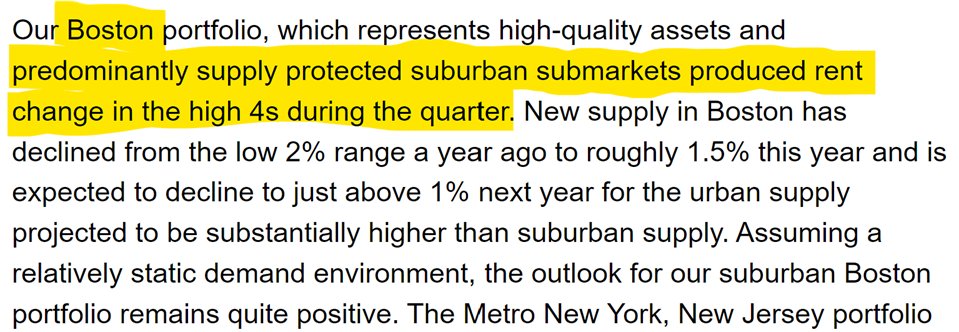

6) AvalonBay noted strength in Boston -- given little competition from new supply, especially in the suburbs. AVB remains bullish on Boston going forward — as its peers seem to be, too.

- Sean Breslin, AvalonBay

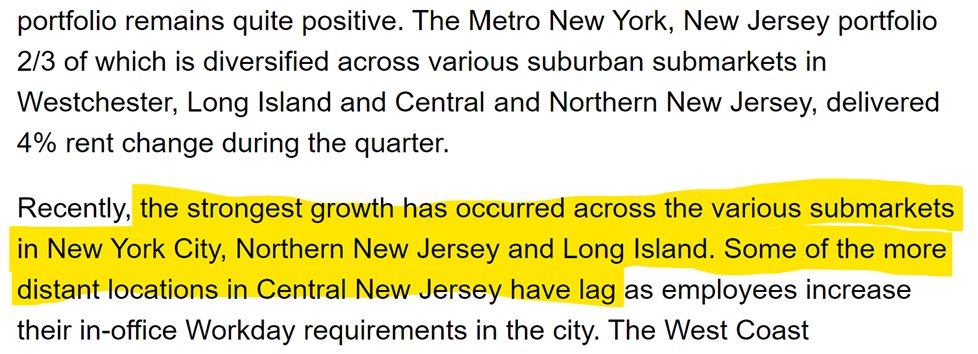

7) Solid numbers in New York area despite the aforementioned bad debt issues, especially in/around city (including Westchester, Long Island and Northern New Jersey) -- while noting softer conditions in Central New Jersey. (Also notably, while going heavily suburban in other markets, AVB has nearly fully exited Connecticut.)

- Sean Breslin, AvalonBay

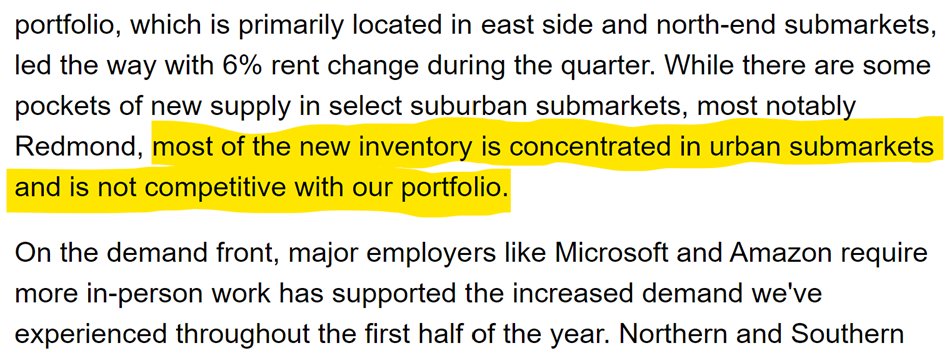

8) Like its peers, AVB highlighted Seattle as top market on West Coast. While noting its presence there is mostly suburban, while most incoming new supply is in/around downtown Seattle area. Seattle’s suburbs have a number of “urban-like” employment and retail nodes that have helped drive appeal.

- Sean Breslin, AvalonBay

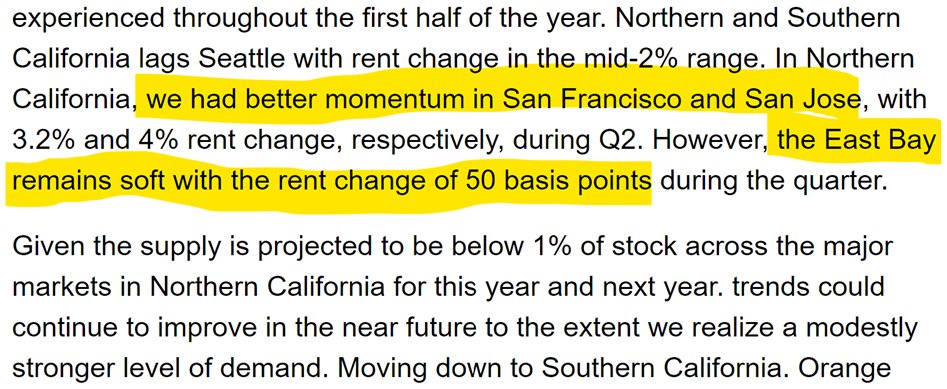

9) AvalonBay reported improving conditions in the Bay Area ... except in East Bay (Oakland area), which has been a persistent soft spot for most apartment operators.

- Sean Breslin, AvalonBay

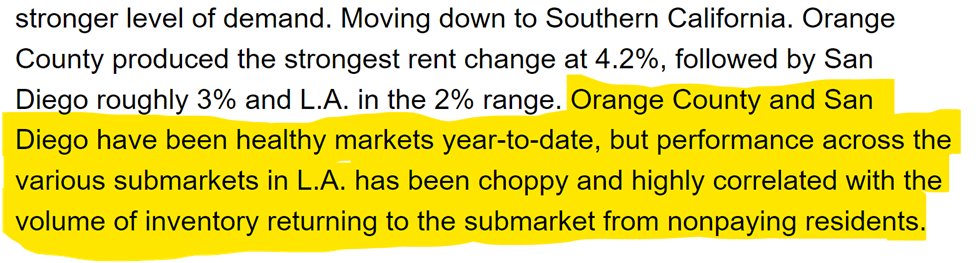

10) AvalonBay sees a mixed bag in SoCal, echoing peers who noted that Los Angeles continues to underperform its neighbors. AVB traced L.A.'s softness, in part, to "the volume of inventory returning from [long-term] nonpaying residents" following the end of an extended eviction moratorium.

- Sean Breslin, AvalonBay

11) Like many peers, AVB reduced its expense guidance following a positive report on expense growth moderation -- led by efforts to reduce on-site headcount and centralize some operations (which is industry-wide point of focus these days).

- Sean Breslin, AvalonBay

12) While noting East Coast outperformance at the moment, AVB (like EQR) doubled down on its Sun Belt expansion plans ... and also continuing a shift toward more suburban > urban. AVB acknowledged “continued challenging levels of new supply” in their Sun Belt expansion markets while noting a shift underway: “We believe we are now moving into a more attractive environment to execute on this repositioning … in our Sun Belt expansion regions.”

Benjamin Schall, AvalonBay

13) AvalonBay is yet another player buying into the view that 5% is the new norm on cap rates, and they're actively buying around that price (and below replacement cost), while it also sold five coastal properties (three of which were urban located).

Matthew Birenbaum, AvalonBay

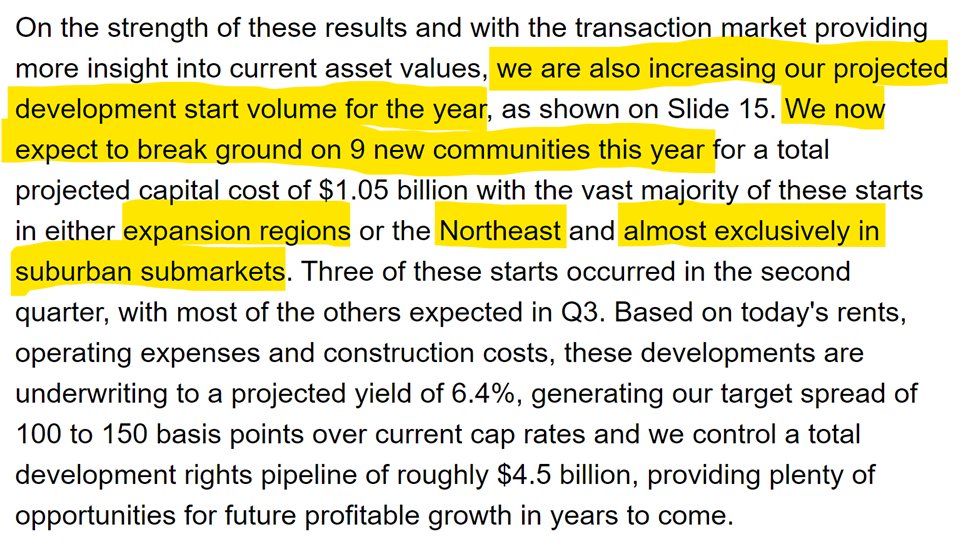

14) AvalonBay offered some rare bullishness on new development (with exception of West Coast, where they said deals don't pencil out). Now expecting to break ground on nine projects this year (up from seven previously planned) -- all Sun Belt or Northeast.

Matthew Birenbaum, AvalonBay

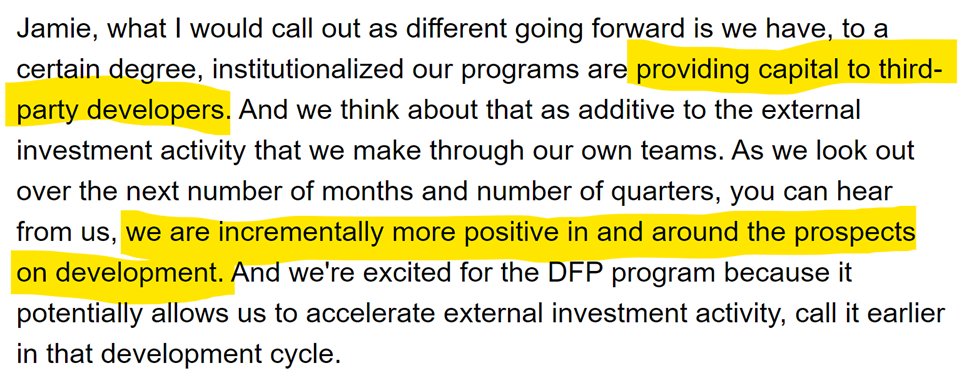

15) AvalonBay is a developer itself but also looking to fund third-party developers -- something similar to what others talked about, too -- to "accelerate" investment activity, presumably entering projects after they've been entitled and are shovel ready.

Benjamin Schall, AvalonBay

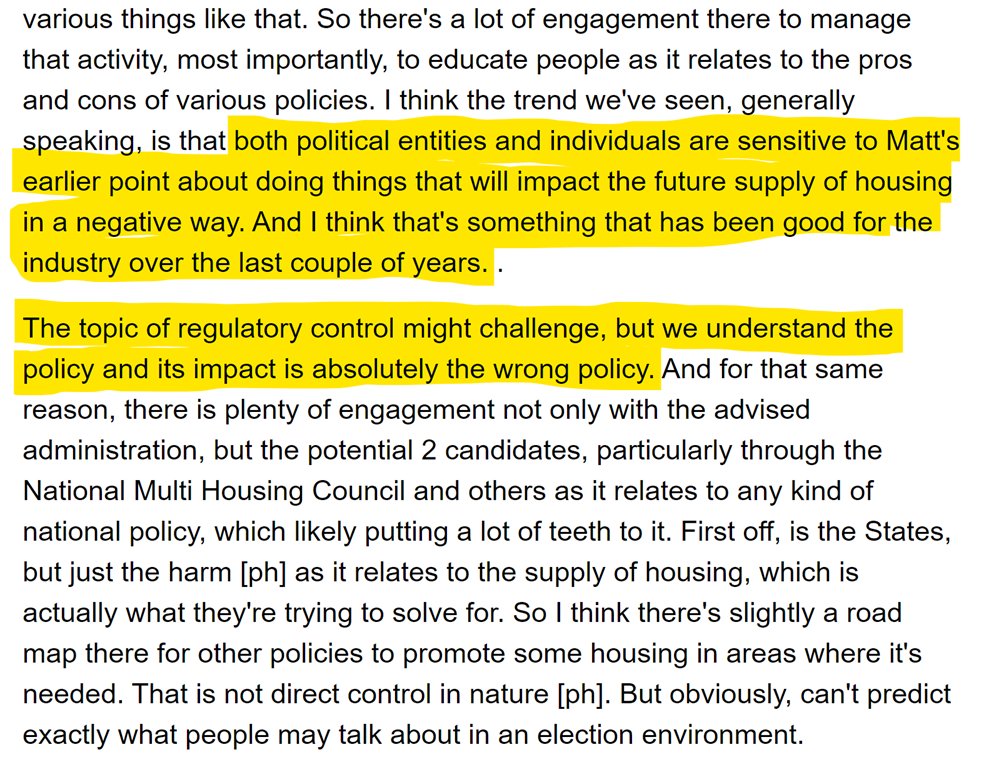

16) Asked about rent control and other regulatory proposals, AVB bluntly pointed out that such policies only further constrain new supply and "that's something that has been good for the industry" (in coastal cities) while at the same time noting it's the "wrong policy."

-Sean Breslin, AvalonBay

Essex Property Trust (ESS)

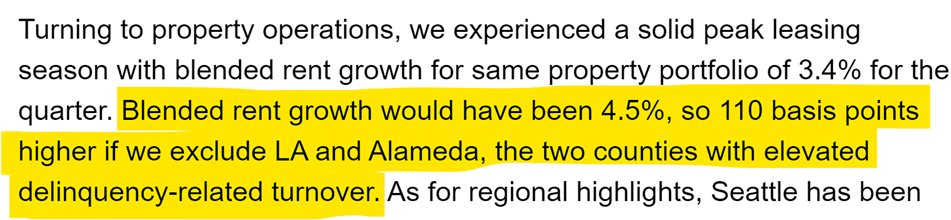

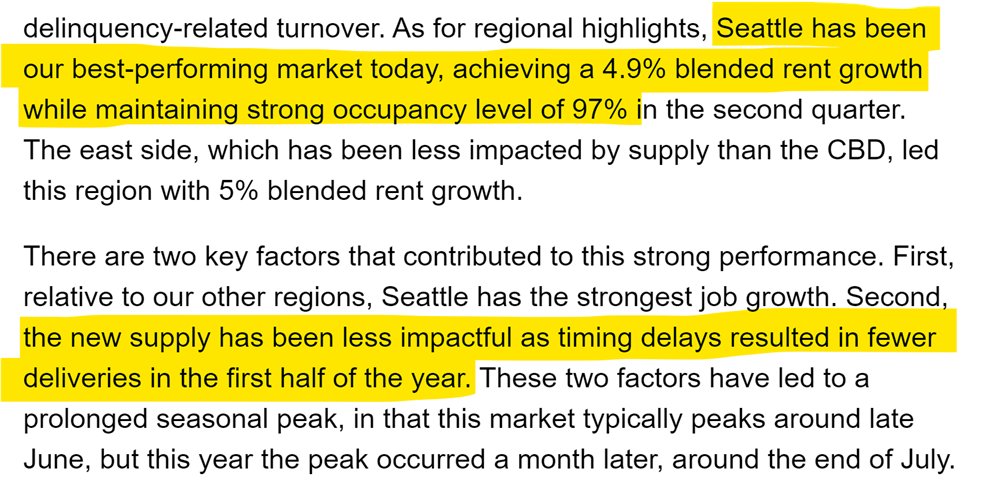

1) Strong growth across the West Coast, with notable exception of Los Angeles and Alameda County (Oakland area). Essex in recent periods has offered up rent growth numbers with L.A. and Alameda removed to highlight their softness relative to the rest of the portfolio. (More on this later.)

- Angela Kleiman, Essex

2) Essex reported Seattle as a standout market (as did others) thanks to strong job growth and delayed apartment construction (a headwind still on the horizon, as EQR noted too).

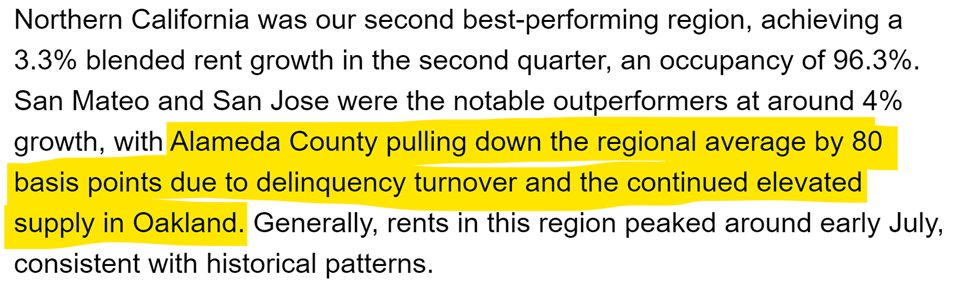

- Angela Kleiman, Essex

3) Also good numbers across Northern California -- especially San Jose and San Mateo. East Bay (Alameda/Oakland) remains weak due to delinquency-related turnover (i.e. slow evictions of long-term nonpayers) plus new supply competition. Tough combo.

- Angela Kleiman, Essex

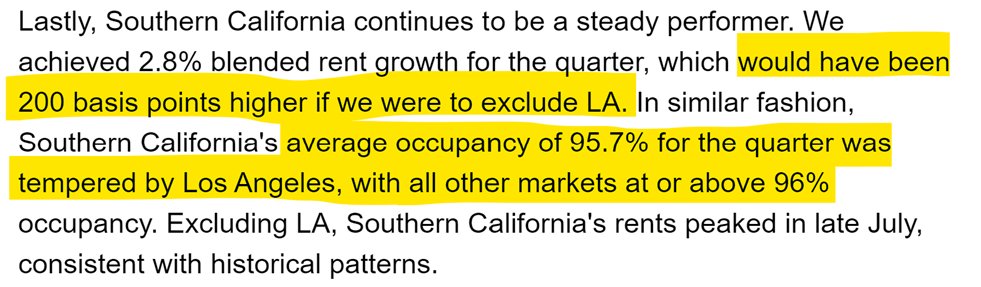

4) SoCal was a similar story with strong numbers outside of one market, Los Angeles. Revenues (not same as rents, fyi) increased ~5%+ year-over-year across San Diego, Orange County and Ventura... but much softer (2.2%) in Los Angeles.

- Angela Kleiman, Essex

5) Essex traced its challenges in both Los Angeles and Alameda County (Oakland) to a "low demand environment" in both L.A. and Alameda on top of "delinquency-related turnover." As an aside, there are pockets of supply pressures in L.A., too, but Essex (which is diversified across asset classes) downplayed supply and instead focused on demand-side challenges.

- Angela Kleiman, Essex

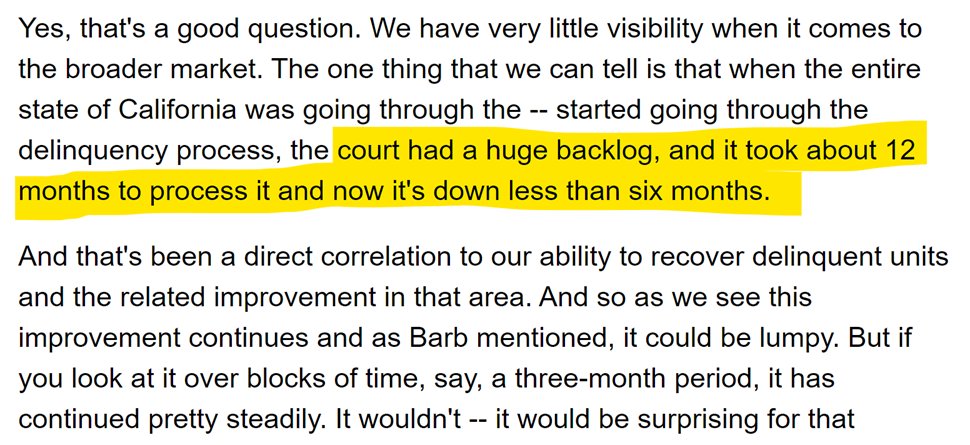

6) But there are signs of real improvement on long-term delinquency issues. Essex earlier this year did report improvement on bad debt (meaning more renters are paying rent), and last week also reported the court backlogs have been cut in half.

- Angela Kleiman, Essex

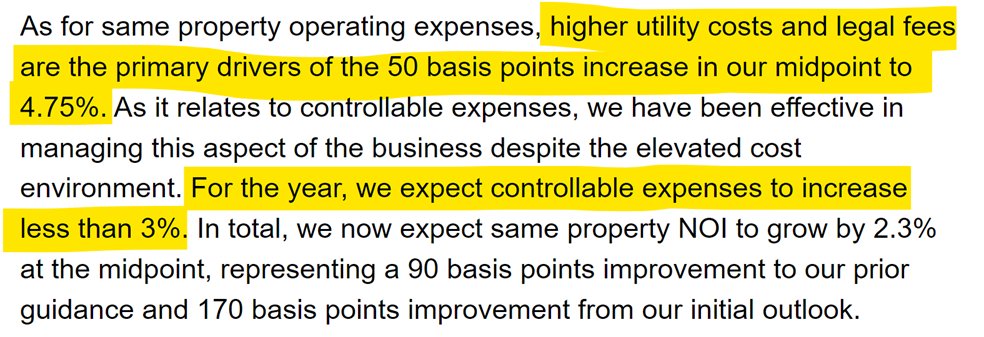

7) Like others, ESS reported expense growth > rent growth, and even while noting positive signs in expense moderation. But unlike most others, Essex pushed up expense guidance a bit due to “higher utility costs and legal fees.”

- Barb Pak, Essex

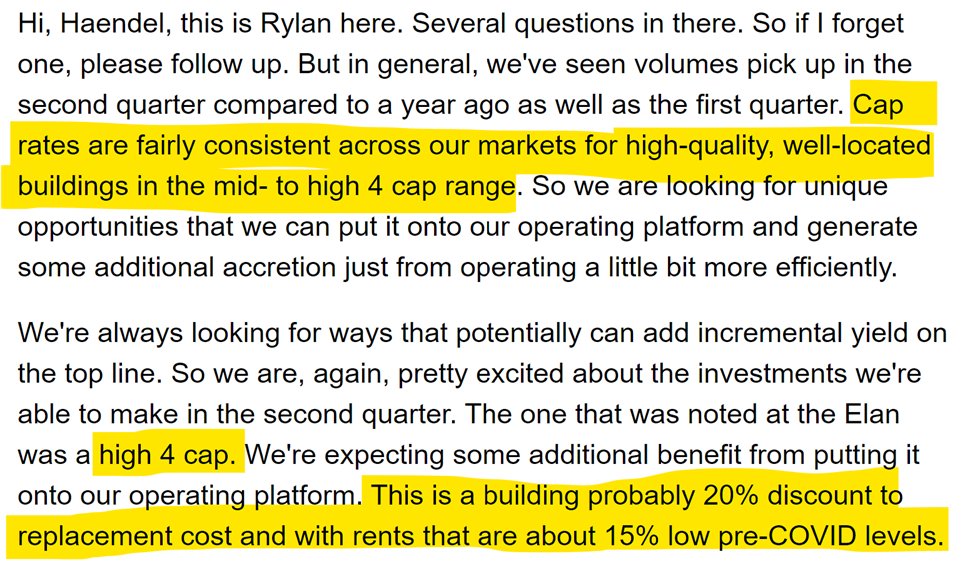

8) Essex said they're finding attractive acquisition opportunities, and noted three recent buys in Bay Area -- highlighting one with a high 4s cap rate, but 20% discount to replacement cost and with rents still 15% below pre-COVID levels.

- Rylan Burns, Essex

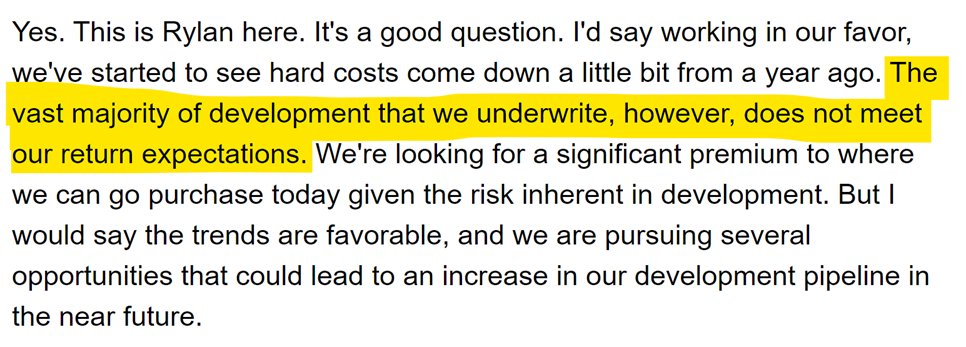

9) Essex said the "vast majority" of (West Coast) new development projects "does not meet our return expectations," which means either costs must drop or rents must rise for more new builds to work. New development is tough to pull off everywhere right now, but especially in the West Coast (no surprise).

Essex said they’ve not started a new project in four years and while they’re open to opportunities, they need to see “at least 100 basis point spread” versus buying existing comparable product.

- Rylan Burns, Essex

10) Overall, Essex seems to expect continued strength everywhere but L.A. and Alameda, where they remain cautious, and did raise full-year guidance for the full portfolio. Also projecting renewal rent increases in the 3.5-4% range.

- Angela Kleiman, Essex

UDR

1) Like others, UDR reported strong financial health among renters. No signs of doubling up, high retention, and rent-to-income ratios of 22%.

- Mike Lacy, UDR

2) UDR saw turnover decline to record low -- which, mirroring industry trend, is perhaps one of biggest surprises of 2024 given volume of new supply competing for renters. "Best second quarter retention in more than a decade."

- Mike Lacy, UDR

3) And they saw strong retention while pushing rents on renewals "just shy of 4%" -- which is in line with overall (not UDR specific) long-term national averages. New leases up just 0.5% --> reflecting competition for new renters.

- Mike Lacy, UDR

4) UDR talked about testing a bit more of a rent push given strong occupancy and renter health, but full-year guidance was more of same on renewals (3.5%-4%) and -1% on new leases.

- Mike Lacy, UDR

5) It's tough pushing new lease rent growth right now (and that's true of nearly everyone, not just UDR) given new supply competition ... and that's despite a massive discount to rent vs. buy. UDR says it's $36k/year cheaper to rent from UDR vs. buy in their markets.

- Mike Lacy, UDR

6) UDR reported notable growth of nearly 9% in the "other income" category, which they said represents 11% of total revenue. Much of the growth traces to building-wide WiFi-- which owners can often bundle/sell to renters cheaper than renters can get independently, so win/win.

- Mike Lacy, UDR

7) Like its peers, UDR reported expenses growing faster than rents -- but expense growth is moderating. Big savings through higher retention = fewer move-outs = reduced costs prepping units for next residents.

- Mike Lacy, UDR

8) Intense focus on leasing fraud prevention. This has been a theme for a while across the industry, and UDR talked about it here. Leasing fraud has accelerated materially in recent years, particularly after eviction moratoria were put in place, where people come in applying with stolen/fake identities, and then never pay rent, and then it takes a long time to remove them.

- Joe Fisher, UDR

9) Like others, UDR reported that the lower-supplied East Coast was its top-performing region -- led by DC area and specifically Northern Virginia. (More supply coming to the DC area unlike other East Coast markets, so keep an eye on that one.)

- Mike Lacy, UDR

10) UDR appears to subscribe to the increasingly prevailing view that apartment asset values have bottomed and cap rates settling around 5%. UDR’s Joe Fisher later noted that, for new development, “absolute yields that we’re seeing available in the marketplace today are actually quite compelling relative to history,” but it’s the spreads that keep UDR “a little bit cautious” on starts.

- Andrew Kantor, UDR

Camden Property Trust (CPT)

1) The always-colorful Ric Campo, Camden’s CEO, opened the earnings call with Tom Petty’s “The Waiting,” and artfully noted that “everyone in multifamily is waiting for something.” Peak supply, normalizing bad debt, rate cuts, property insurance/tax relief, buyer/seller standoff, etc. — and some of those things are actually starting to happen.

- Ric Campo, Camden

2) Like others, Camden reported that market-rate rental affordability (at least the A/B market where REITs and institutions operate) has materially improved, with a rent-to-income ratio of 19%. This remains a theme across REITs (and private operators, too) that isn’t getting a fraction of the attention it deserves.

- Ric Campo, Camden

3) Also like others, Camden reported a big decline in renter turnover. Renters are renewing their leases, even with normal-ish renewal rent increases close to 4%. I’ve mentioned this as a surprise them across the sector, but it’s especially notable in high-supplied markets (like many Camden markets) given renters today have a lot more options — and often at discounted rents.

- Alex Jessett, Camden

4) Not surprisingly, some of that decline in turnover traces to low move-outs to home purchase... though I don't think that's the only factor. As I've noted with other REITs, there's been an industrywide focus on retention, "protecting the back door."

- Ric Campo, Camden

5) Supply is "limiting rent growth in most of our markets now," but Camden sees some signs that supply pressures will mitigate. (Camden operates in a large number of cities, with heavy concentration in high-demand, high-supplied Sun Belt markets.)

- Ric Campo, Camden

6) In particular, Camden highlighted Austin and Nashville as "our most challenged markets," which isn't surprising given that these are two of the highest-supplied large markets in the country. Camden gave a rather candid view that in those spots, supply headwinds will stretch into mid-2025, although I wouldn’t interpret that as commentary on all Sun Belt markets. Also key to note “historic levels of new absorption” coming to these same markets.

- Keith Oden, Camden

7) Like its peers, Camden remains bullish on Sun Belt for long term while noting current outperformance on the coasts as well as a couple exceptions like Southeast Florida, Houston and Denver. (More on Houston and DC in the next bullet point.)

- Keith Oden, Camden

8) Camden shared some interesting insight calling out Washington DC (no surprise) and Houston (mild surprise?) as strong markets "leading the portfolio of late." As I noted going into 2024, Houston is a market that could surprise on the upside. Relative to its size, Houston is building much less than its Sun Belt peers in this cycle — and its construction rate actually trails the U.S. average.

- Keith Oden, Camden

9) Camden is seeing pretty healthy occupancy rate of 95.5% despite the high supply pressures ... in part thanks to strategy to drop new lease rents to win demand. Occupancy is always key.

- Keith Oden, Camden

10) One thing to watch: loss-to-lease (gap between what new renter pays versus current renter), down to 1%, and with gain-to-lease situation in Nashville and Austin -- which likely makes retention more difficult in those spots. This is a topic to watch not just for Camden, but the industry as a whole — as loss-to-lease has narrowed significantly across most of the country. Ultimately (and there is some seasonality to this that plays a role, too) operators need some acceleration in new lease rents or it becomes more difficult to keep pushing on renewal rents.

- Alex Jessett, Camden

11) On the plus side for Camden, like others, expense growth is moderating and they lowered expense guidance for 2024. One key factor: Insurance premiums (which skyrocketed in prior years) came in DOWN 3% compared to initial projection of +18%.

- Alex Jessett, Camden

12) Another positive: Camden (like Sun Belt peer MAA) sees low bad debt -- meaning renters are paying rent on time every month. Noted a couple challenges in California and Atlanta, but even there the numbers have improved and returning close to the pre-COVID norm. This is one metric where Sun Belt markets are still outperforming most coastal markets.

- Alex Jessett, Camden

13) With starts plunging, even in the Sun Belt, Camden is getting a bit more bullish on new development again -- starting two new projects in Charlotte and (like its peers) also looking to partner with financing-challenged developers with shovel-ready projects.

- Ric Campo, Camden

14) "Land prices tend to be stickier than you would think." Camden offered some good color on the market to buy land for development, noting "just like the sellers of existing multifamily," land sellers are "unwilling to drop their prices.”

- Ric Campo, Camden

15) Lastly, kudos to the analyst who put the ball on the tee for Camden CEO Ric Campo to opine on how Wall Street values apartment REITs like Camden. (I’m sure the analyst knew where this was going.)

- Ric Campo, Camden

Independence Realty Trust (IRT)

1) IRT continues to “see pressure from new deliveries,” while noting “apartment absorption outpaced historical levels.” Furthermore IRT expects supply in their submarkets to begin declining in the second half of 2024.

- Scott Schaeffer, IRT

2) Like others, IRT is feeling the short-term supply > demand in key Sun Belt markets, calling out Atlanta, Nashville, Raleigh/Durham, Huntsville (and elsewhere also mentioned Austin and Charlotte) while noting these same markets outperform on population and jobs. IRT also has a presence in the Midwest region, which has been a top region for apartment operators given very limited new supply competition.

Asked about Atlanta (a key market for IRT), IRT reported improving trends in both rents and in leasing fraud prevention / bad debt, noting “we’re definitely moving in the right direction.”

- Janice Richards, IRT

3) But it’s not a demand issue, with lead volumes (prospective renters) up 25% year-to-date compared to the same period last year. IRT gave some of the credit to not only job/population growth, but also “refined marketing strategies and increased spend on lead generation.”

4) IRT reported strong gains in both occupancy (+120 bps) and in resident retention (+160 bps) year-over-year, while at the same time reducing concessions. Instead of concessions, IRT relied on bottom-line rent cuts on new leases. (More on that in next bullet point.)

- Mike Daly, IRT

5) New lease rents fell “due to the continued supply pressure,” but IRT said they “do not expect this trend to continue” with fewer upcoming lease expirations in the portfolio plus strong leasing traffic.

6) IRT lowered its revenue guidance a bit “due to the lower blended rental rate growth we’ve experienced year-to-date as we focus on improving resident retention and occupancy.” But IRT did also report that new lease and renewal lease rents are both showing material improvement so far in Q3.

- James Sebra, IRT

7) Like others, IRT is still seeing solid returns from renovations despite the supply pressures. IRT expects to do a good bit more renovations in the second half of the year than they did in Q1.

- Scott Schaeffer, IRT

8) Like others, IRT reported continued improvement in the share of renters paying rent every month. Bad debt fell 40 bps to 1.6% year-over-year.

- James Sebra, IRT

9) IRT now expects expenses to grow significantly less than previously expected for 2024. IRT credited declines in property taxes and insurance premiums, as well as reduced repairs and turnover costs thanks to lower turnover.

- James Sebra, IRT

10) Property insurance premiums declined 10%, after previously being expected to increase by 17.5%. That’s a big shift — reflecting a sea change in the multifamily property insurance markets.

- James Sebra, IRT

Next Up on REITs’ Q2 Earnings:

Also reporting last week: American Homes 4 Rent, Elme Communities, Clipper Realty. Due to length of this newsletter, I am saving those four for the next edition.

This Week: BSR, Bluerock

In last week’s newsletter: Invitation Homes, Equity Residential, Centerspace, NexPoint Residential, Veris Residential.

I’ll continue posting observations from earnings call first on X/Twitter @jayparsons (as well as shorter recaps on LinkedIn) and then will compile/expand in upcoming newsletters.

Thank you to the sponsor of this newsletter, Madera Residential. Click the image above to learn more about Madera’s multifamily platform.