- Jay Parsons' Rental Housing Economics

- Posts

- Highlights from First 5 REIT Earnings Calls

Highlights from First 5 REIT Earnings Calls

First five SFR and Multifamily REITs to report: Invitation Homes, Equity Residential, Centerspace, NexPoint Residential, Veris Residential

Jay Parsons

July 31, 2024

Sponsored by: Madera Residential

It’s earnings call season for the single-family rental and apartment REITs. Lots of great color gets shared during these earnings calls. This newsletter covers the first five to report: Invitation Homes, Equity Residential, Centerspace, NexPoint Residential and Veris Residential. Future newsletters will cover highlights from other REITs’ earnings call.

As always, this commentary is not investment advice (nor should it be interpreted as such) — just stuff I found interesting.

Invitation Homes (INVH)

1) Property taxes spiked 10.3% (especially in Florida and Georgia) – which is a key factor for long-term affordability in those markets – but that’s being "partially offset by lower turnover."

- Charles Young, INVH

2) Resident turnover is declining not only because of low move-outs-to-purchase, but also because of improved "bad debt lease compliance" -- which means many long-term nonpayers from COVID era have moved out and now a higher share of residents paying rent each month.

- Charles Young, INVH

3) For move-outs due to “lease compliance” (i.e. long-term non-payer), turnover costs are 50% higher than a “normal” move-out. That’s a pretty notable stat. For those not familiar with the lingo, “turn costs” reflect costs to clean/repair/prep the rental home. INVH is suggesting that there’s more residents paying rent today, which means fewer “lease compliance” move-outs, and therefore reduced turn costs.

- Jon Olsen, INVH

4) Summer temps peaked earlier this year, which meant higher-than-expected HVAC costs.

- Charles Young, INVH

5) Invitation continues to focus on growing their SFR portfolio through new BTR home construction -- contributing net positive growth in housing supply. Pipeline up to 2.7k new homes on top of 2k already built.

- Dallas Tanner, INVH

6) Occupancy remains higher than normal, even as rent growth continues to normalize and seasonality comes back. (Seasonal patterns kind of disappeared during the pandemic era.)

- Charles Young, INVH

7) Invitation thinks rent growth has peaked for the year, and they "expect to continue to lean on occupancy" to drive revenue growth. (A reminder that empty units = zero revenue, despite the persistent conspiracy theories we hear about on social media.)

- Charles Young, INVH

8) Normal seasonal patterns are returning. This gets a bit technical but it's a key point. Seasonality sort of went away (for both SFR and multifamily) in the pandemic era, but it’s becoming increasingly clear that normal seasonality is returning as the market normalizes. This means the return of seasonal patterns in demand, loss-to-lease and pricing.

- Charles Young, INVH

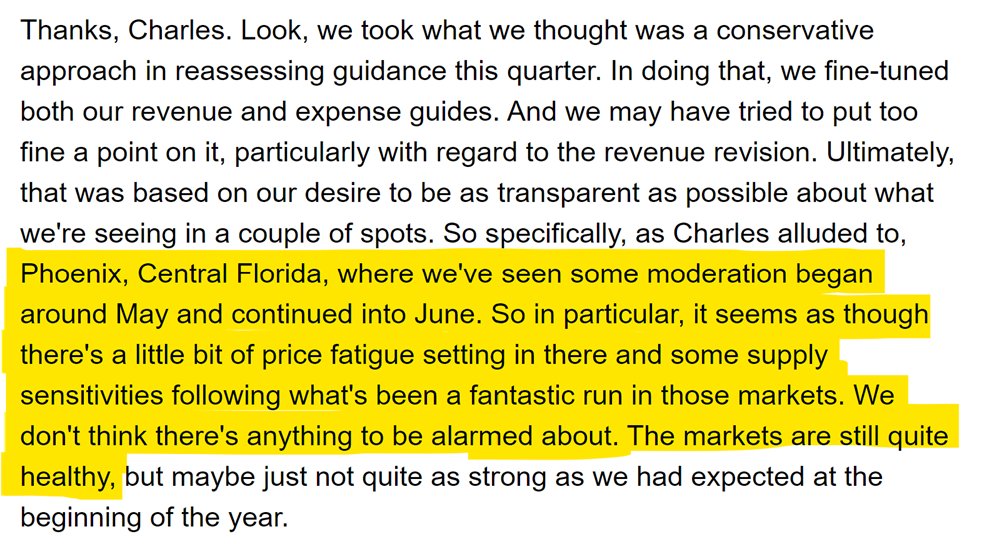

9) Invitation called out Phoenix and Central Florida as slower than other markets. Noted "price fatigue" and "supply sensitivities," which usually means (my interpretation) that even when affordability isn't an issue, renters are simply finding better deals in the market.

On the flip side, Invitation noted continued strength in other markets, including Chicago and SoCal... and perhaps most surprisingly, early signs of renewed momentum in Atlanta.

- Jon Olsen, INVH

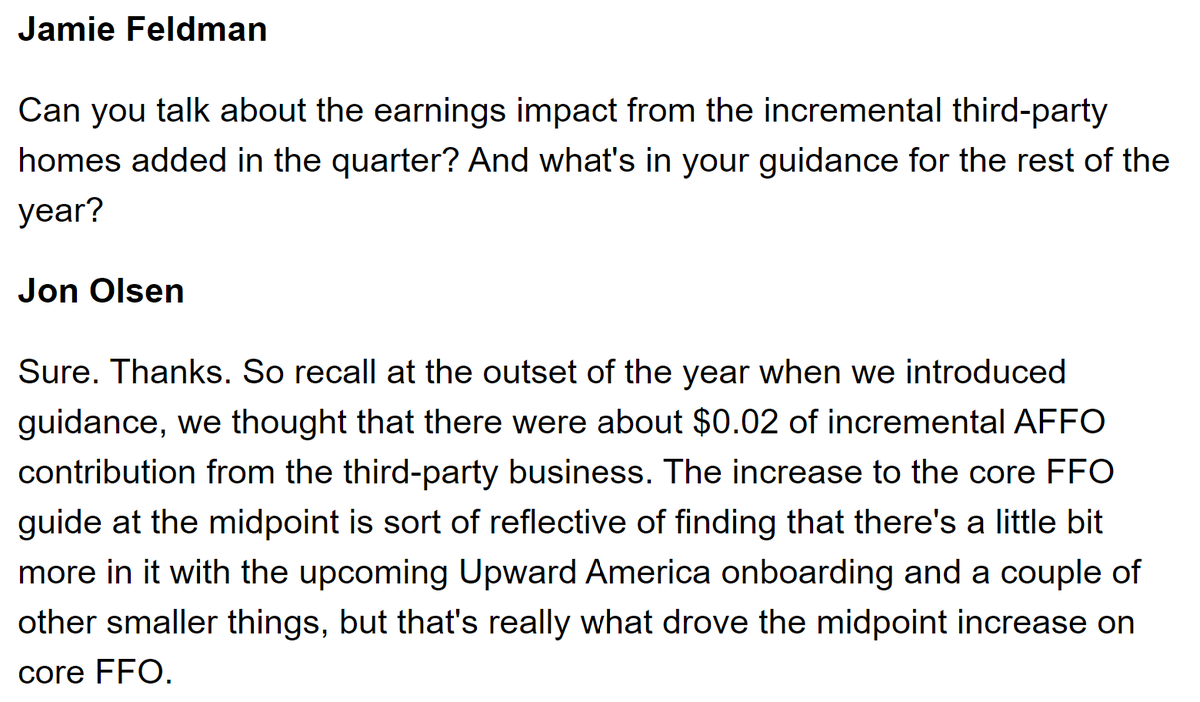

10) Invitation reported gains in its previously launched third-party property management platform (which means managing SFR homes on behalf of other owners), and highlighted upcoming onboarding of Upward America.

- Jon Olsen, INVH

Equity Residential (EQR)

1) Strong demand -- both for new and renewal leases -- from renters in strong financial position, echoing themes we continue to hear from REITs and even private sector owners, too. Rental affordability (and demand at today’s rent levels) is a much more bifurcated issue than it’s generally understood to be. (More on this later.)

- Michael Manelis, EQR

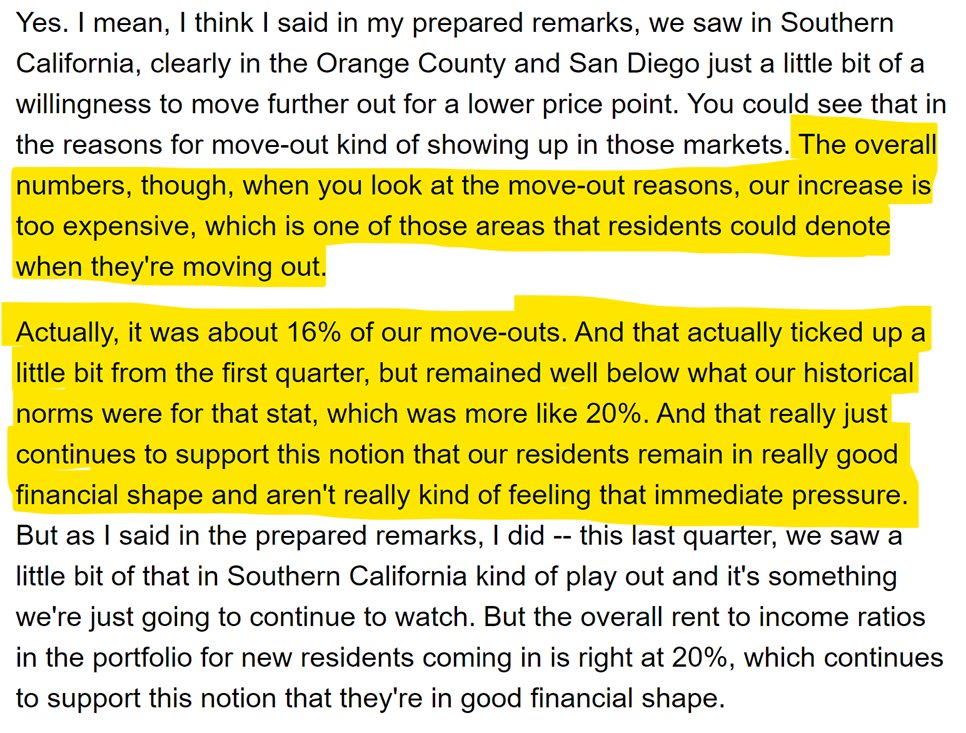

2) Move-outs due to rent increase remain below normal (16% vs. 20%), but EQR did see an uptick of move-outs for affordability reasons in parts of SoCal.

- Michael Manelis, EQR

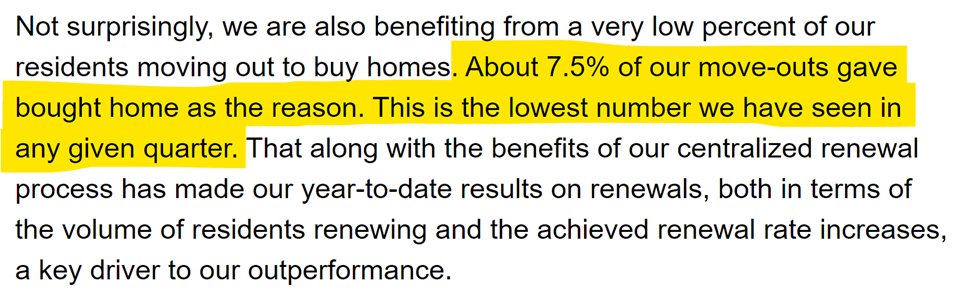

3) Like other REITs, EQR continues to report very low move-outs to home purchase given today's high rates. In fact, Q2 was lowest on record at just 7.5% of move-outs being for home purchase. EQR is also seeing value in centralizing/streamlining renewal process.

- Michael Manelis, EQR

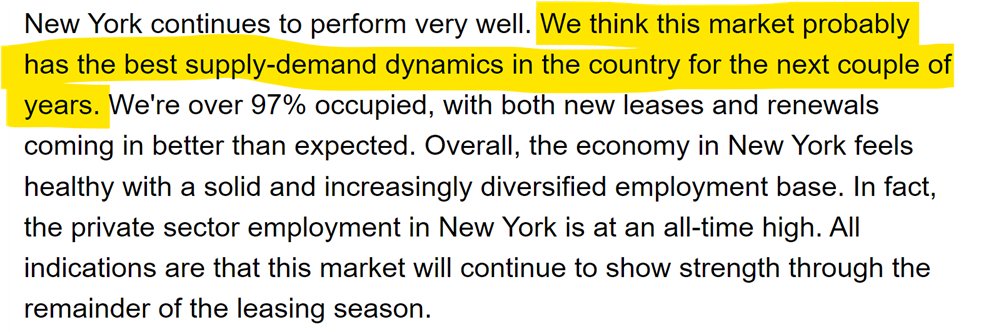

4) East Coast remains the top-performing region at this point in the cycle (lower supply than West Coast or Sun Belt), and EQR singled out New York City's rebound (especially at top end of market where they operate) and imbalanced supply/demand picture (i.e. city's inability to stimulate more housing).

Also highlighted Boston and Washington, DC, as strong performers — while noting upcoming supply hitting the DC market.

- Michael Manelis, EQR

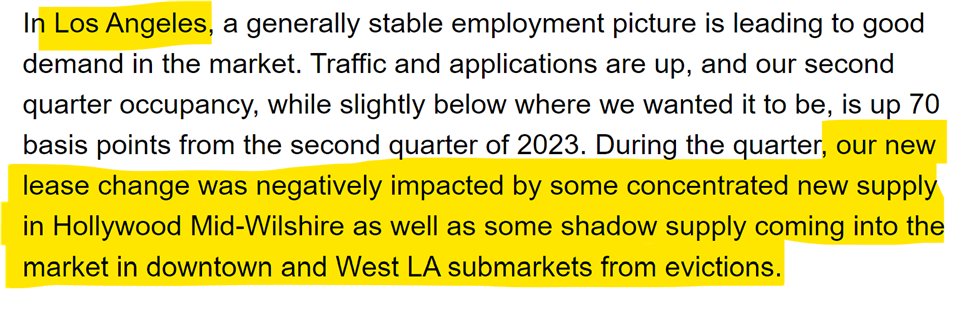

5) Conditions remain softer on the West Coast, and EQR singled out Los Angeles as (my words, not theirs) still a weaker spot due to high supply (something people don't talk about enough in LA's Class A market) and the eviction backlog.

EQR did not improvement in San Francisco and Seattle (specifically calling out improved “quality of life issues"), while cautioning about upcoming supply wave in Seattle. Seattle is a bit unique in that its supply wave is backloaded (2H’24-1H’25) compared to most other markets.

- Michael Manelis, EQR

6) Sun Belt markets, with higher supply, are “performing in line with expectations” but EQR remains committed to expansion in the region. EQR re-emphasized its plans to allocate a growing share of its portfolio to the Sun Belt (+Denver). Like others, EQR sees improving picture in 2026-27 as supply drops off "much lower than both current levels and historical levels" and then benefits of podding operations.

- Mark Parrell, EQR

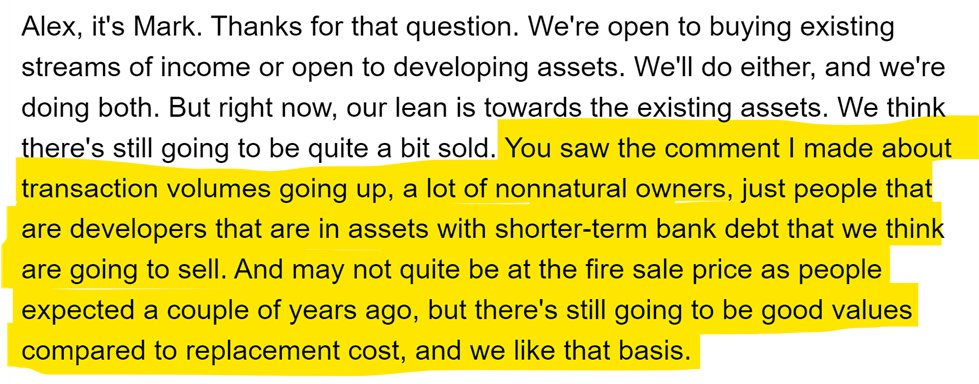

7) Like others, EQR’s acquisition strategy targets newer construction in the Sun Belt. They’re not expecting "fire sale prices," but finding "good values compared to replacement cost."

- Mark Parrell, EQR

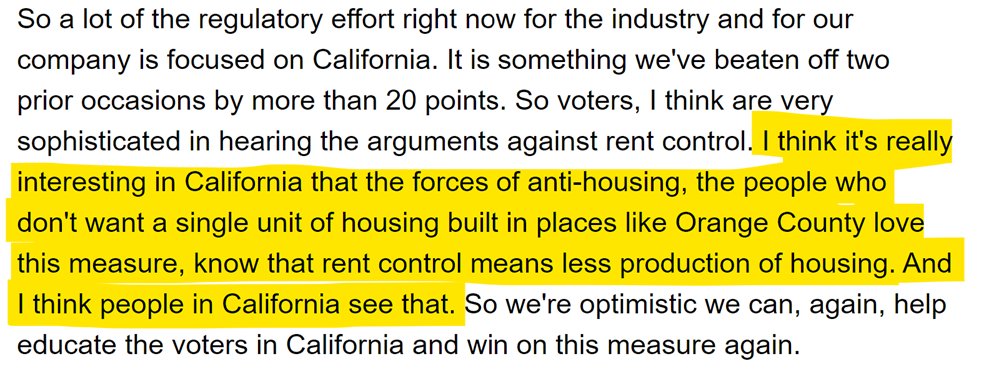

8) EQR is ramping up for another ballot measure vote over rent control expansion in California -- after CA voters overwhelmingly (and wisely) shot down the prior ballot measures, noting its obvious negative side effects on renters.

- Mark Parrell, EQR

9) Like others, EQR seeing good signs on expenses and revised down its expense guidance by 100 bps. Reported improvement primarily in repairs/maintenance, payroll and utilities. Payroll is a particularly interesting one to call out. If that holds across the industry, it could suggest the hiring/retaining talent market could be normalizing.

- Robert Garechana, EQR

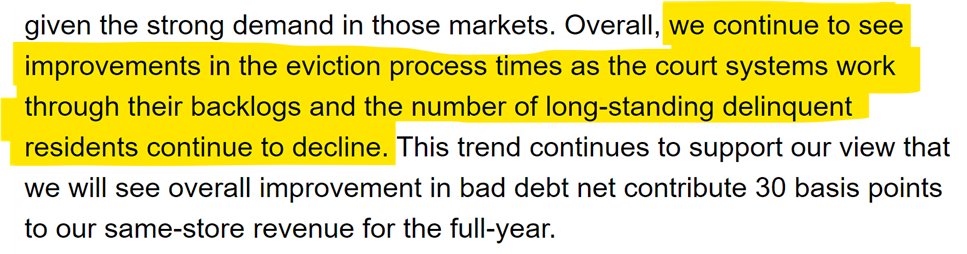

10) EQR reported "improvements in the eviction process times as the court systems work through their backlogs and the number of long-standing delinquent residents continue to decline."

- Michael Manelis, EQR

11) EQR said they expect to see some moderation in renewal rent growth as spreads tighten between new leases and renewals.

Generally speaking (not specific to EQR): New leases are still priced above renewals on a nominal basis, but have been flat/negative on percentage change basis — even as renewal rents have increased. So the spreads are compressing. If you start pushing renewal rents above the rent levels listed for new renters on your website, retention tends to get challenging.

- Michael Manelis, EQR

Centerspace (CSR)

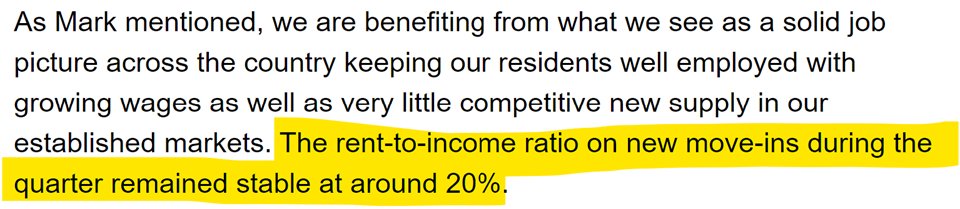

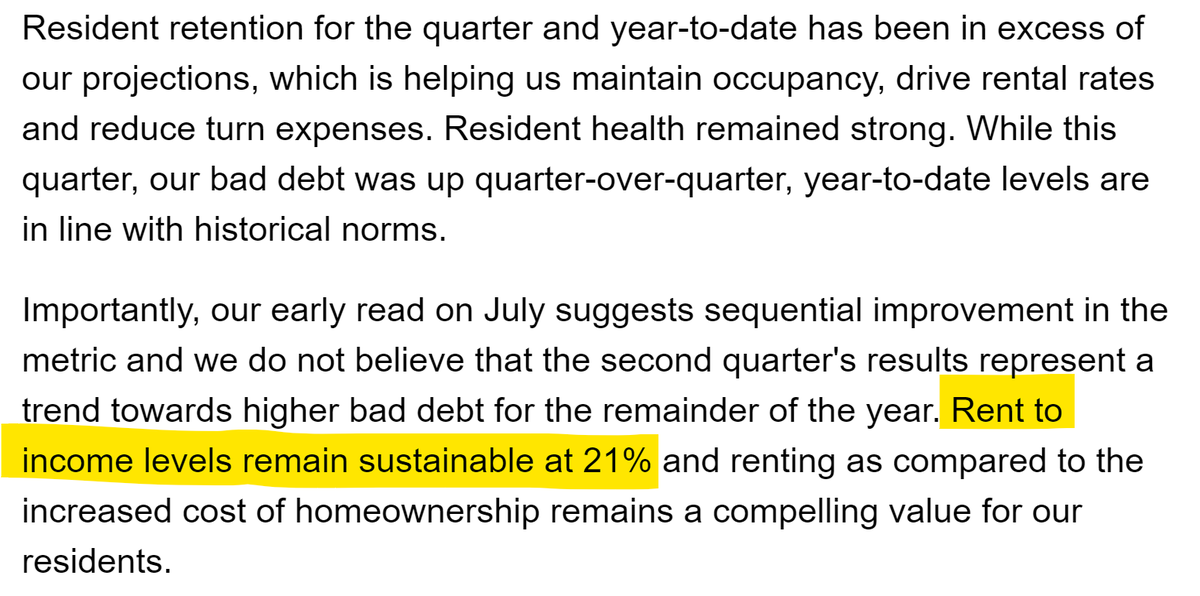

1) Like others, Centerspace reported very healthy financial health among its renters. Higher-than-expected resident retention, back-to-normal rental delinquency rates, and healthy rent-to-income ratios of 21%.

- Anne Olson, Centerspace

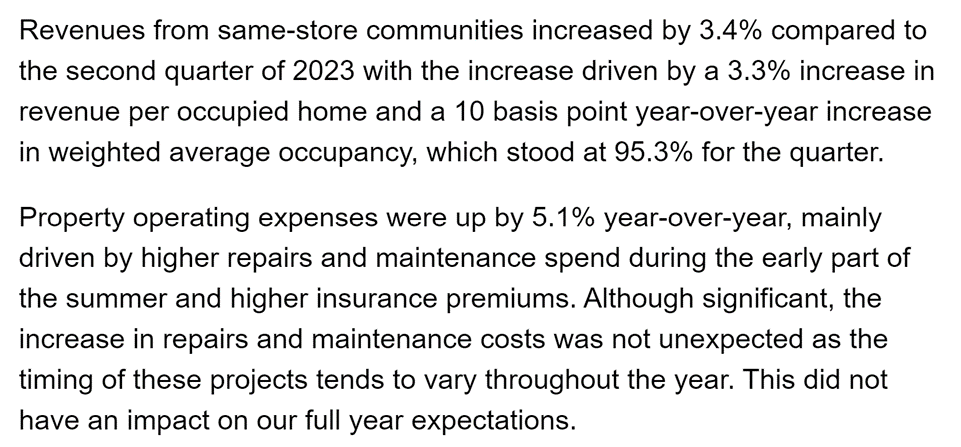

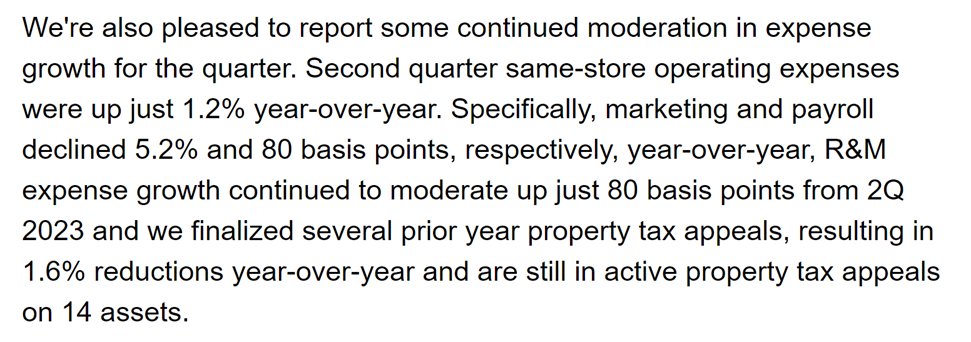

2) Expenses are still growing faster than revenues (even in the low-supplied Midwest!), but expenses are trending in the right direction and Centerspace lowered their guidance on projected expense growth.

- Bhairav Patel, Centerspace

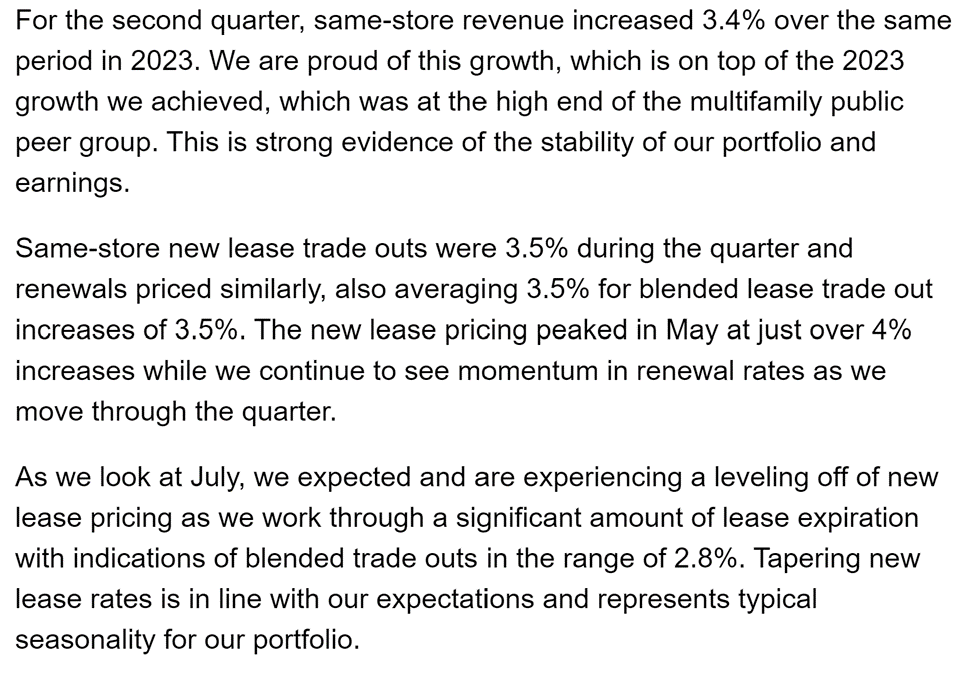

3) Centerspace reported solid rent growth as you'd expect to see given their geographic footprint (primarily outperforming, low-supply markets), while noting they expect normal seasonal tapering for remainder of year.

- Anne Olson, Centerspace

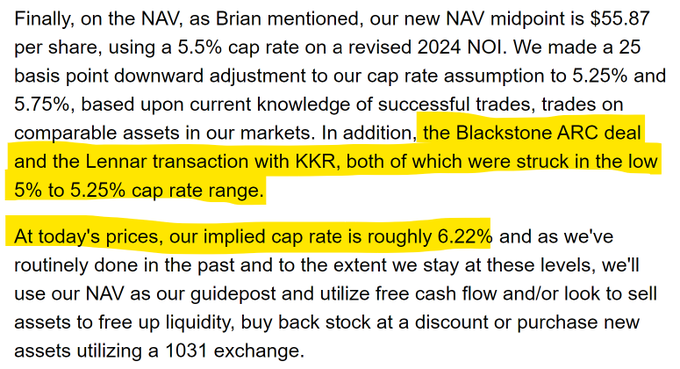

4) Centerspace signaled renewed interest in potential acquisitions after a long lull, joining the chorus of voices suggesting that prices are settling in the 5% cap range (give or take based on location, type, etc.)

- Anne Olson, Centerspace

5) Most value-add projects at this point are tech related, and specifically smart home tech (which typically don't require taking units offline for construction) and they're seeing residents willing to pay a premium for it, while also reducing costs.

- Anne Olson, Centerspace

NexPoint Residential Trust (NXRT)

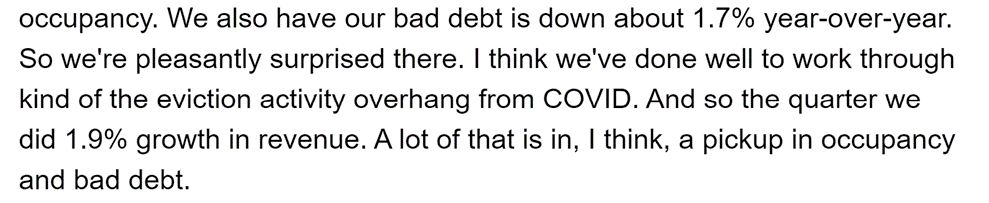

1) Like others, NexPoint reported strong retention and healthy resident financial health. Strong resident retention rates, though with minimal renewal rent increases, helping boost occupancy rates in supply-heavy markets.

- Matt McGraner, NXRT

2) High volume of competitive new supply, but also strong demand. NXRT is in higher-supplied Sun Belt markets. Renters there have more options so will pick better deals even when/if affordability is non-issue.

One positive: "Demand really outperformed expectations ... and was really exceptional on a historical basis."

- Matt McGraner, NXRT

3) NXRT is still seeing strong ROI on renovations / value-add upgrades. Impressive because it's a tougher environment today to pull this off given volume of supply putting downward pressure on rents, and availability of newer product competing for renters.

- Brian Mitts, NXRT

4) Like other REITs, NexPoint is seeing reduced bad debt — meaning a larger share of residents are paying rent — and reported progress working through COVID-era backlog of non-paying residents.

- Bonner McDermett, NXRT

5) Also like other apartment REITs, NexPoint reported further moderation in expense growth. OpEx inflation trailed rent inflation in this cycle, so expenses have been growing faster than revenues of late for many apartment operators.

- Matt McGraner, NXRT

6) NexPoint is working through large refinancing program through Freddie Mac to mitigate some of the impact of today's higher rates -- and projecting positive impact to bottom line. Likely to see a lot of this in private sector too. Positive sign for industry health.

- Matt McGraner, NXRT

7) NXRT -- like its peers -- noted the continued large gap between how Wall Street values Sun Belt apartment REITs versus how the private sector values Sun Belt apartment assets. (And who can blame them?)

- Matt McGraner, NXRT

Veris Residential (VRE)

1) Veris reported a remarkably low rent-to-income ratio of just 12% among households signing a new lease in Q2. That’s despite Veris operating luxury apartments in some of the nation’s priciest submarkets of New York, Northern New Jersey and Boston. They did report the average, and it’s possible — though just speculation — the median could be closer to the ~20% norm of most REITs.

Either way, it’s yet another data point showing how rental affordability is deeply bifurcated. Speaking broadly (not specific to VRE), rent level and affordability tend to be inversely correlated — meaning renters in higher-priced Class A rentals tend to spend a lower share of income on rent simply because they tend to have high incomes. Inversely, renters in lower-priced rentals (much of which is not institutionally owned) tend to spend a higher share of income on rent.

- Mahbod Nia, Veris

2) Veris reported acceleration in rent growth, which partly reflects a relatively small portfolio by REIT standards (<8k units) uniquely concentrated at the very top end of the market in a few low-supplied cities.

- Mahbod Nia, Veris

3) Veris pulled out of a planned acquisition due to concerns that it’d be “unintended signaling” that the management team might be prioritizing external growth over “organic value-creation opportunities.”

Not sure exactly what that means, and they didn’t offer up a ton of detail. Asked about it later in the earnings call, the management team eluded to “a subset of investors” concerned about the “unintended signaling,” and called it a “misunderstanding.”

- Mahbod Nia, Veris

Next Up on REITs’ Q2 Earnings:

Last night: Essex, UDR

Today: MAA, AvalonBay, IRT

Tomorrow: American Homes 4 Rent, Camden, Clipper Realty, Elme Communities

Next Week: BSR, Bluerock

I’ll be posting observations from earnings call first on X/Twitter @jayparsons (as well as shorter recaps on LinkedIn) and then will compile/expand in upcoming newsletters.

Thank you to the sponsor of this newsletter, Madera Residential. Click the image above to learn more about Madera’s multifamily platform.