- Jay Parsons' Rental Housing Economics

- Posts

- Apartment REITs Earnings Call Recaps, Part 2

Apartment REITs Earnings Call Recaps, Part 2

Highlights and market color from MAA, UDR, Essex, IRT, NexPoint and Veris.

Jay Parsons

November 21, 2024

Sponsored by: Madera Residential

This is the third (and final) in a series recapping highlights from Q3’24 earnings calls among the rental housing REITs. Today’s edition covers the remaining six (alphabetically) apartment REITs: Essex, IRT, MAA, NexPoint, UDR and Veris.

Last week, we covered the first seven apartment REITs: AvalonBay, BSR, Camden, Centerspace, Clipper, Elme Communities and Equity Residential. And prior to that, we covered the two big single-family rental REITs.

Another shameless plug before we dive in: Check out “The Rent Roll with Jay Parsons” podcast for more on the REITs on your streaming platform of choice (Apple, Spotify, YouTube, Amazon, etc). This week’s episode (released today) features the Top 5 takeaways on the apartment REITs plus a conversation the former CEO of Centerspace multifamily REIT, Mark Decker. Last week’s podcast featured an interview with the CEO of Invitation Homes, Dallas Tanner, plus takeaways from the SFR REITs’ earnings calls.

***Lastly: As always, this commentary is not investment advice (nor should it be interpreted as such) — just stuff I found interesting.***

Essex Property Trust (ESS)

West Coast portfolio with 62k units

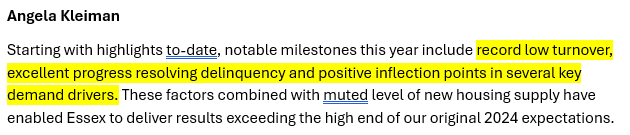

1) Essex ramped up the bullishness, most notably calling out "excellent progress resolving delinquency" -- which had been problematic, especially in L.A.

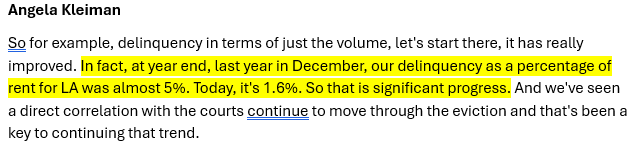

2) More details on improvements in renters paying rent: L.A. delinquencies down from 5% of rent to now 1.6% as courts work through the eviction backlog (mostly very long-term delinquencies built up during eviction moratoria).

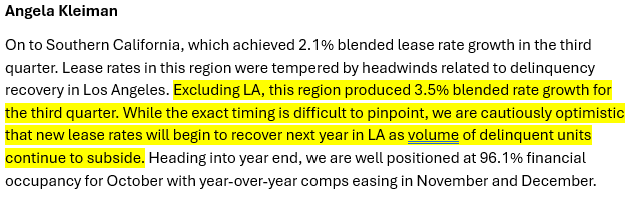

3) Still, Essex (like others) continues -- for now -- to single out L.A. (and Oakland/Alameda County) as outliers pulling down performance, while being "cautiously optimistic" about L.A. recovery next year.

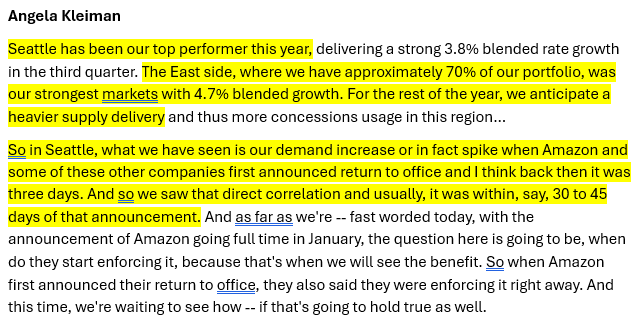

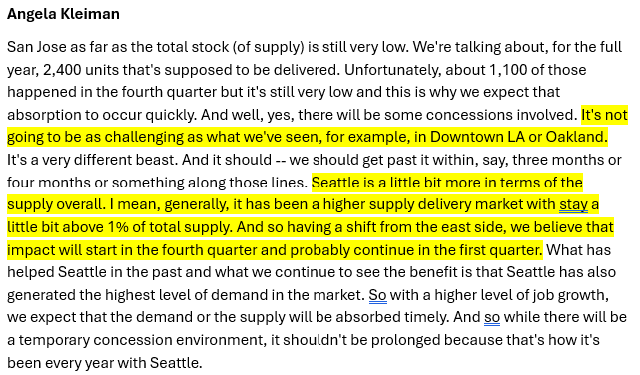

4) Seattle remains the top-performing market (and not just for Essex) thanks to strong demand drivers. Essex -- like its peers -- reported a clear boost in leasing traffic following Amazon's return-to-office announcement. Also notes high supply could be headwind in next few quarters.

5) Northern California (especially Silicon Valley) remained a regional bright spot, too. Essex credited return-to-office policies here, too, as well as increased tech job postings.

6) Essex noted that while supply is less a factor in many of its submarkets, there are some big exceptions like Downtown LA, Oakland, parts of Seattle and (for a moment) San Jose.

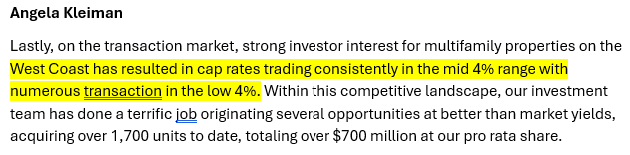

7) Essex (which, as a REIT, has lower cost of capital than most other players) has been active buyer this year-- even with cap rates falling back into the low 4s in some cases.

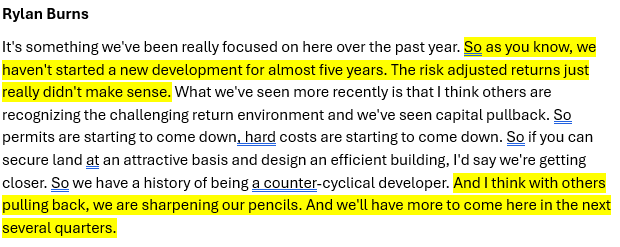

8) Essex still isn't doing any new development (and hasn't in almost 5 years!) because "the risk-adjusted returns just really didn't make sense" -- a term every pro-housing YIMBY should be familiar with. BUT ... Essex hinted it could get active. "We are sharpening our pencils."

9) One reason little new housing is built on the West Coast is, of course, the policy environment. And on that note: Essex said it's spent $16mm so far this year and expects to spend $30mm in 2024 on advocacy -- mostly to oppose California Prop 33, presumably. (Prop 33 was the rent control expansion ballot measure that voters soundly rejected.)

10) The ESS earnings call occurred prior to Election Day, and Prop 33 was defeated by a big margin, but pre-Election Day, Essex took view that most CA cities wouldn't rush toward extremist, anti-science rent control policies due to inevitable consequences on renters, and that most legislators "understand the impact" it would have. (Indeed, many elected officials — including Democrat Gov. Newsome — opposed Prop 33.)

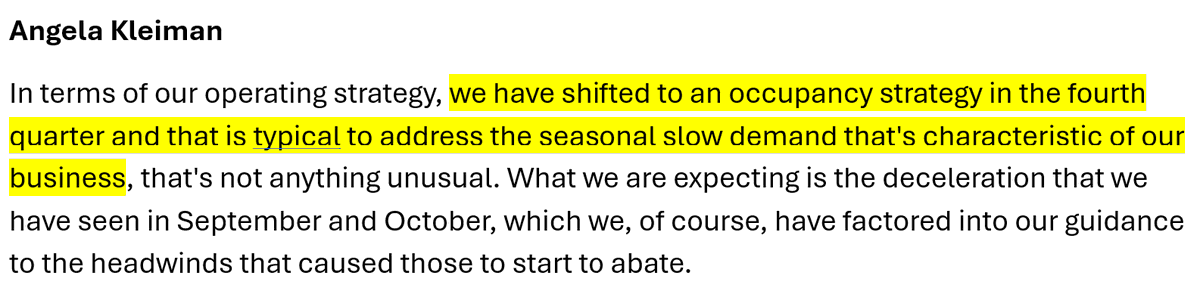

11) Back to operations. One thing you'll hear from all the REITs this time of year is that leasing velocity and rents slow down over the winter months. Normal seasonality.

12) But seasonality has less impact on renewals, which continue to grow near 4%, in part thanks to low turnover -- broadly mirroring industrywide trends across the country.

Independence Realty Trust (IRT)

Sun Belt, Mountain and Midwest portfolio with 32k units

1) Like others, IRT is feeling the impact of high supply on new lease rents. New lease trade-out measured -3.6%, which IRT attributed to “pressure from new supply.” But IRT also believes supply is peaking and that new lease rent momentum will return in 2025. Even suggested that they’re “seeing signs” of improvement in asking rent.

2) Also like others, it’s a much more positive story on the renewal leasing side. Renewal trade-out measured 3.8% in the quarter, and looks like even better momentum in early part of Q4 thanks to still-healthy occupancy rates and low turnover.

3) IRT sold one property (in Birmingham) and bought one (in Tampa), plus it’s under contract to buy three more: two lease-ups (in Charlotte and Orlando) and one stabilized deal (in Columbus, OH). Reported unusually high cap rates blending at 5.7%. (More on that in a moment). Bought with only 35% leverage (not many buyers can do that today).

4) IRT was asked how they found deals in the upper 5s — which is a good question, since other REITs reported trades in mid-to-high 4s. The answer: They’re buying lease-ups pre-stabilization, with occupancy rates in the low 80% range when they went under contract, thereby “willing to take some lease-up risk.” Still, on the surface (and for full disclosure: I know nothing about these deals), that seems like favorable pricing given the low leverage and the nearly stabilized occupancy rates. It’s the profile a lot of other buyers are looking for right now.

5) But ground-up development remains off the table for IRT — which makes them different from their peers in the Sun Belt and Mountain regions.

6) On expenses, IRT reported a mixed bag: higher costs for salaries and maintenance, but lower costs in property taxes and insurance. Blamed sticky “inflationary pressures” for the former, while notching some big savings on the latter — including a 10% reduction in insurance premiums earlier this year.

7) Add IRT to the list of REITs reporting challenges in Atlanta, BUT … there were also some signs of improvement. Blended rents were negative in Q3, but positive in October. And perhaps more encouragingly, occupancy improved 240 bps year-over-year. However, “we will still see challenges with bad debt” / fraud.

8) Still pushing forward on value-add renovations, with weighted average returns in the 15-16% range. Planning to complete 1,700 unit renovations this calendar year.

Mid-America Apartment Communities (MAA)

Primarily Sun Belt portfolio with 104k units

1) New supply at peak levels, but MAA reported better-than-expected occupancy, retention, collections and expenses -- but did see continued new lease rent cuts.

2) New rents were down 5.4%, and yet renewals still increased 4.1% due to strong renewal demand -- which remains (industry-wide) a remarkable upward surprise given volume of new supply competition. Occupancy ticked up 20 bps to 95.7%, and renters are paying the rent each month.

3) Crazy stat: Austin is such a tough market right now (due to massive supply wave) that MAA said if they excluded Austin from their portfolio, new lease rent momentum from Q2 to Q3 would have been +10 bps instead of -30 bps. Also noted Atlanta as tough market w/ supply, too.

4) Austin aside, MAA took a bullish stance on impact of 50-year high in supply dinging NOI by -1.3%. "If that's as bad as it gets, that's okay. And next year will be better. '26 will be even better. I think '27 and '28 will be even better."

5) MAA said secondary markets with lesser supply pressures are helping lift overall performance, specifically calling out Savannah, Richmond, Charleston, Greenville and Fredericksburg.

6) One interesting stat MAA noted several times was that 60-day exposure is at record low of 6.3%. This is called lease expiration management (match availability with demand). Only a small share of leases are expiring during the seasonally slow winter, protecting occupancy.

7) MAA reported no real damage from recent hurricanes, primarily just landscaping cleanup. That was true of other REITs, too.

8) MAA says institutional portfolios like theirs are not materially impacted by shifts in immigration. One analyst asked MAA about impact of potentially reduced immigration on apartment demand, leading to an interesting exchange and this comment from Eric:

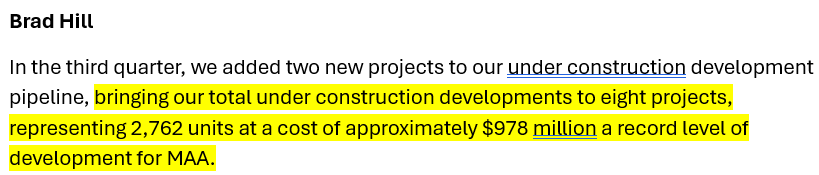

9) Ramping up the construction engine again. While total apartment construction is cratering, MAA is ramping up construction to "record level"(starting projects in Charlotte and Richmond) to take advantage of reduced supply environment by time projects deliver in 2026-27. Another 10 projects in pipeline.

Before anyone takes that comment to assume apartment starts will ramp up again, it's important to note that REITs like MAA are tiny share of market and are uniquely positioned w/ cash on hand / low cost of capital. Most developers have to raise $ and take on pricier debt. (I wrote about this in last week’s newsletter, too.)

10) MAA is also an active buyer (again uniquely positioned as REIT), primarily focused on acquiring recently built apartments in the Sun Belt -- buying in Orlando and Dallas. Now reporting cap rates in high 4s (down a tick) for newer Class A apartments. This aligns with strategies from other big REITs, too.

11) More detail on MAA's acquisition strategy-- trying (like others) to take advantage of slow lease-up velocities and financing challenges.

12) MAA implied some cautious bullishness on 2025. Supply will remain elevated, but down from 2024's peaks. Winter months are seasonally slow, but MAA expecting "a little more positive momentum in terms of new lease pricing" by Q2/Q3 2025.

NexPoint Residential Trust (NXRT)

Sun Belt portfolio with 13k units

1) Like others, NXRT is feeling impact of high supply, with new lease rents down 6.4%. Expecting to “remain defensive” (i.e. rent cuts) next couple quarters but suggests improvement in 2025.

2) Also like others, NXRT is benefitting from strong renewal demand – allowing renewal rents to climb 2.2% even as new lease rents fell. Strong retention + new lease rent cuts helped maintain occupancy near 95%, which is still healthy rate.

3) NXRT appears to be feeling more expense pressures than other REITs. Even with relatively low turnover, NXRT reported high turn costs. (Remember: Turnover is expensive!) Expecting improvement to come given higher occupancy and reduced turnover.

4) NXRT continues to report good returns on renovations – which is a positive for NXRT because renovations are not always automatic returns, especially given supply competition as you go more upmarket / higher rent.

5) NXRT sold a 1998-vintage Houston property in October at a reported 5.25% cap rate. Seeing 1990s vintage apartments trading in low 5s seems representative of today’s market.

UDR, Inc. (UDR)

National portfolio with 60k units

1) Lots of talk on using customer data to improve retention strategies, and some good hard numbers on impact: UDR estimates that "for every individual we save, it's approximately $5,000." Reducing turnover by 1,800 units in last 12 months "translates to about $9 million in NOI" for UDR. That’s based on improving turnover by 200 bps year-over-year and by 600 bps versus their 10-year average.

2) That’s part of UDR’s ongoing project to learn from “hundreds of thousands of daily touch points” to improve the living experience, retention and capital expense.

3) On fundamentals: Similar themes as others, with new leases negative (-2%) and renewal leases up (+>5%).

4) Are widening spreads between new and renewal leases sustainable? This has been theme across industry, and what it means is a potential gain-to-lease scenario where renewing renters are asked to pay more than a new renter. One analyst asked the question of UDR. Insightful answer from Mike Lacy, who noted he’s monitoring that datapoint closely, but so far is encouraged by high retention rates and lack of move-outs blamed on rent increases.

5) UDR reported a healthy occupancy rate of 96.3% in Q3, but that was still “lower than our historical average.” UDR says that was “strategic” due to focus on implementing “enhanced AI screening and fraud detection” to protect against long-term bad debt / rental delinquency. More on that in a moment…

6) UDR took the view that (modestly) higher bad debt is the new reality. And to be fair: We’re still talking about very low numbers — with bad debt (long-term rental delinquency) in the low 1% range instead of the 0.4-0.5% range where it was pre-COVID. These aren’t apocalyptic numbers by any means. UDR said it’s not because there are more bad actors, but because “it takes a lot longer to get them out” due to increased regulatory restrictions.

7) But renter health, more broadly, remains strong. “Rent-to-income ratios really haven’t changed” since 2019, and apartments have only become more affordability relative to buying homes.

8) While some other REITs are increasingly active buyers and builders, UDR is taking a “capital light” approach for now. They’re seeing greater value in stock buybacks given public valuations coming in well below net asset values based on where properties are trading today.

9) Also, UDR is investing more on renovations than on development, and seeing good opportunities for “refreshing the portfolio and trying to get the consumer a better product, also raising the NOI profile.”

10) Like others, bundled/bulk wifi remains a big win/win — delivering ancillary revenue to UDR while providing discounted internet to residents. It added $5 million in NOI in 2024, and could be “close to double that next year.”

11) UDR will likely shift back into starting new ground-up developments in 2025. The math is still difficult due to rate volatility and rent softness, but “we’re getting close.” UDR says they’ve got “a number of good parcels and projects that are shovel-ready and ready to go.”

12) On operations, East Coast remains the top performer (same as other REITs), while the West Coast is seeing some bounce back thanks to return-to-office mandates. Sun Belt still pulled down by supply pressures. (More on that next.)

13) Like others, UDR is optimistic rent growth could return to the much of the Sun Belt in 2025 thanks to mitigating supply pressures. UDR pins the rebound to mid-2025 in Denver, Dallas, Tampa and Orlando, while the higher-supplied Austin and Nashville may take longer (late 2025 or into 2026).

Veris Residential (VRE)

Northeast portfolio with 7.6k units

1) Veris is benefitting from exposure limited to only lower-supplied markets in New York, New Jersey and Massachusetts, with new lease growth of 1.3% and renewals at 6.5%. Still interesting to see widen splits in new versus renewal pricing, similar to the bigger / national REITs.

2) Veris continues to report some very impressive numbers on renter demographics and affordability, with rent-to-income ratios at 12% and average household incomes of $388,000.

3) Veris talked about its results from using AI leasing tools to improve conversion rates and reduce payroll costs — strategies popular across the industry these days. Some critics worry such things would lead to reduced resident satisfaction, but Veris reported steady improvement in reputation scores.

***As a reminder once again: None of what I write about REITs (or otherwise) is intended to be investment advice whatsoever, nor is it a comprehensive look at any REIT. I just write about the things I find interesting.***

***Now Spinning on the Podcast***

We launched a podcast! Find us on YouTube, Spotify, Apple and Amazon. The Rent Roll with Jay Parsons.

Episode 1: The Case for Middle-Income Housing with special guest Bob Simpson, head of the Multifamily Impact Council

Episode 2: Debunking a Few Multifamily Myths with BSR REIT CEO Dan Oberste

Episode 3: The Hurdles for Apartment Builders with Payton Mayes, CEO of JPI

Episode 4: Fresh Data and REITs’ Earnings Previews with REIT researcher David Auerbach.

Episode 5: Win/Wins for Cities and Developers with Bellevue Mayor Dr. Lynne Robinson

Episode 6: The Politicalization of Rental Housing with ex-Fannie Mae CEO Hugh Frater

Episode 7: Rental Housing 2024 Voters’ Guide with ex-Freddie Mac CEO David Brickman

Episode 8: The Case for New Apartment Construction with Thompson Thrift CEO Paul Thrift

Episode 9: SFR REITs’ Q3 Earnings Recaps & Outlook with Invitation Homes CEO Dallas Tanner

***Released today: Episode 10: Apartment REITs’ Q3 Earnings Recaps & Outlook with ex-CEO of Centerspace REIT, Mark Decker***

Thank you to the sponsor of this newsletter, Madera Residential. Click the image above to learn more about Madera’s multifamily platform.