- Jay Parsons' Rental Housing Economics

- Posts

- Apartment REITs Earnings Call Recaps, Part 1

Apartment REITs Earnings Call Recaps, Part 1

Highlights and market color from AvalonBay, EQR, Camden, Elme, Centerspace, BSR, Clipper

Jay Parsons

November 15, 2024

Sponsored by: Madera Residential

This is the second in a series recapping highlights from Q3’24 earnings calls among the rental housing REITs. Today’s edition covers the first seven (alphabetically) apartment REITs: AvalonBay, BSR, Camden, Centerspace, Clipper, Elme Communities and Equity Residential.

Yesterday’s edition (which you can find here) covers the two big single-family rental REITs. And the third and final edition (coming early next week) will cover the remaining apartment REITs.

Shameless plug before we dive in: Check out The Rent Roll with Jay Parsons podcast for more on the REITs on your streaming platform of choice (Apple, Spotify, YouTube, Amazon, etc). This week’s episode (out now) features a Top 5 takeaways on the SFR REITs plus a conversation with Invitation Homes CEO Dallas Tanner. Next week’s episode (dropping Nov. 21) will break down the Top 5 takeaways for the apartment REITs and feature a conversation with the former CEO of Centerspace multifamily REIT, Mark Decker.

***Lastly: As always, this commentary is not investment advice (nor should it be interpreted as such) — just stuff I found interesting.***

AvalonBay (AVB)

National portfolio with 93k units, primarily coastal suburban.

1) Don't bet against renters in institutional market-rate apartments. AVB says renters are in financially strong shape w/ income growth outpacing rent growth again across the U.S.

2) Bad debt (long-term delinquency) continues to improve, though still a bit elevated in markets (generally that had long-term eviction moratoria) including New York, DC and Los Angeles. Healthier in Boston, Northern VA, Orange County, San Diego.

3) AvalonBay continues to see stronger revenue growth in Boston, New York City, DC area and Seattle. Softer in Northern California, Denver and Florida / other Sun Belt markets (with heavier doses of new supply competition).

4) Like its peers, AvalonBay is seeing a improved demand stemming from return-to-office mandates, particularly by Amazon in Seattle and Salesforce in San Francisco.

5) AVB continues to ramp up new development. Remember that REITs have major advantage over merchant builders because they have more cash and lower capital costs, so AVB (and others) see opportunity in starting projects when most builders can't do as much.

6) Projects that work right now to be "simpler" -- low-density garden apartments. AVB started four projects in Q3, two in Texas and two in North Carolina. Eyeing other markets across U.S., too.

One of those starts is in Austin, which led to an analyst asking why do that deal given supply saturation there? Interesting answer from AVB, noting long-term play for "signature community" that could eventually total 1,300-1,400 units.

7) When AVB (and others) start a new project, they say they’re assuming untrended rents -- which means they use today's market rent values for initial lease assumptions. That means fewer deals pencil out in a flat-to-falling-rent environment, but for those that work, it means there's upside.

8) AVB has sold more than they've bought this year -- though would like to buy more, but market remains thin. AVB (correctly, in my view) noted that hopes for accelerating deal flow hit a wall as treasuries ticked back up.

9) AVB is generally selling older properties in coastal markets and buying newer properties in Sun Belt markets -- primarily suburban. This is part of AVB's strategy to reach 25% allocation in Sun Belt (+Denver) to follow growth and balance "regulatory exposure" risk on coasts.

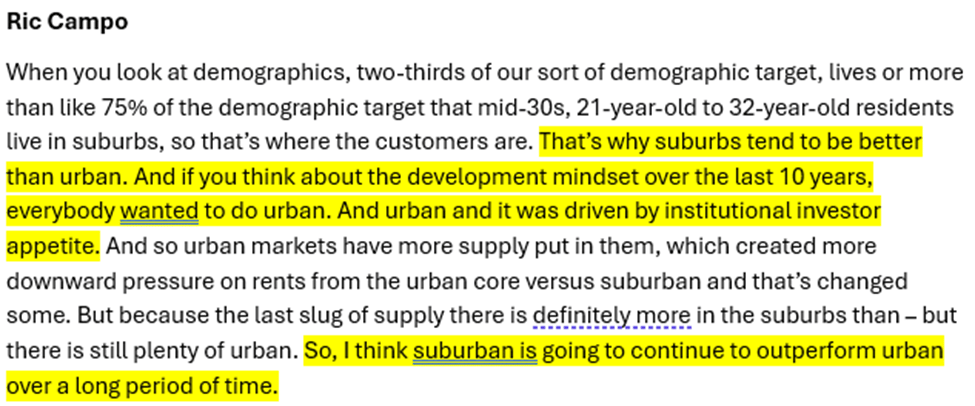

10) AVB was early believer in the suburbs -- countering what was (in years past) the conventional thinking that urban was better. They're targeting the "aging millennial" in high-barrier suburban locations across their markets. AVB is now 73% suburban. (Camden talks about this, too.)

11) AvalonBay likes BTR. Build-to-rent (particularly townhomes, a sort of hybrid apartment/SFR product type) is an area of increased focus as part of AVB's suburban strategy. That type of product potentially allows AVB to reach families with kids, who are less likely to rent traditional apartments.

12) Back to operations: Renter turnover remains low, mirroring an industrywide trend. AVB attributed that, in part, to "record lows" in move-outs to purchase homes. (But as I’ve noted many times before, don’t give the slow for-sale housing market all the credit. There was a lot of intentionality among property managers across the industry to boost retention this year, and it’s largely worked.)

BSR REIT

Sun Belt portfolio, especially Texas, 9k units

1) Like others, BSR believes their markets are peaking on supply. Supply looks likely to decline, even as demand tailwinds remain strong. Dan Oberste said: "The absorption of this supply has exceeded our expectations and the pace of new development has slowed dramatically.”

2) Also like peers, new lease and renewal lease rents are a bit inverted. New lease rents fell 2.5%, while renewal rents climbed 2.6% thanks to still-strong retention rates plus healthy occupancy near 95%. Just as MAA reported, Austin is a drag on BSR’s portfolio rents too.

3) BSR wants to be a buyer, but there just aren’t many sellers/opportunities out there yet. Like others, BSR is targeting new construction (even those still in lease-up) and still bullish on Texas as supply drops off. Colorful language from Dan on "the gazelle we're hunting."

4) Like others, BSR thinks supply will be much lower in coming years due to headwinds facing developers. (Of course, the data supports this view, too.) BSR thinks debt is too expensive for developers, and many will also have to first recycle capital by selling off recent builds as they stabilize.

5) Revenues climbed in part due to ancillary categories like utility reimbursements. But that was countered by higher tax expenses.

Camden Property Trust (CPT)

National portfolio with 60k units, mostly Sun Belt

1) It's tough to build because "construction costs have NOT come down and rents HAVE come down. And while Camden is moving forward on a few new projects (see next point), they believe those opportunities will be limited — even for REITs with lower capital costs.

2) That said, Camden plans to start 2-3 projects next year (Denver and Nashville) that still work. But … they've also shelved projects in California, Buckhead/Atlanta and urban Houston -- as CPT works (on previously announced plans) to reduce exposure in all three spots (and in DC, too).

3) Camden wants to be more of a buyer than a builder in the current market. More development is possible but would require "outsized" future rent growth to pencil out. Outsized rent growth is in line with third-party forecasts, but CPT doesn't want to assume it as base case.

4) Camden thinks the acquisition market will really ramp up in 2025-26 as merchant builders move to unload a heavy volume of recent lease-ups + banks nudge certain borrowers to sell as values rebound. CPT will be looking to buy suburban over urban.

5) More on urban vs. suburban in a moment, but first: Camden made it clear it's not a bargain shopper's market. The distress that's out there isn't REIT-quality product, and CPT would rather buy newly built apartments from merchant builders (which other buyer want, too).

6) "There's more buyers than sellers" so Sun Belt Class A cap rates have compressed back into the 4s. But pricing is still below replacement cost and with reduced supply pressures moving forward, that underwriting is "pretty comfortable." Where will CPT be buying? Note the tease for the Q1 earnings call, when CPT plans to lay out their plans for future geographic diversification.

7) Those deals just haven't been there yet, so Camden hasn't been active buyer in 2024 but "expect us to be more active in '25 and '26 for sure." CEO Ric Campo (as he often does) also noted CPT's stock price trading at a discount relative to private market asset values.

8) On operations, it was a familiar story: New supply pressures are pushing new lease rents negative, but strong retention allowing for solid renewal rent growth. Top markets for revenue growth: SoCal, DC, South Fla, Denver, Houston.

9) Longer term, it remains clear Camden is NOT a believer in Los Angeles. LA has been a drag on most REIT portfolios (due to mix of fraud, evictions, demand, supply). But while their peers express optimism, CPT says "L.A. has a demand problem" and not just for the short term.

10) Another market where Camden plans to reduce some exposure (but remain very present) is Houston, but for very different reasons. Great demand story, but CPT is tiring of sees investors pin its stock based on swings in oil prices due to Houston's reliance on energy sector.

11) Back to urban vs. suburban: Camden sees suburbs as long-term better bets, and currently sees suburbs outperforming by 80 bps. I think that's broadly true nationally, too, and a big reason other REITs and institutions have bet heavily on suburbs in recent years.

12) Why do suburbs perform better? It varies by MSA, but IMHO it's a mix of factors (less supply, less turnover, and typically lesser regulatory hurdles on the operations side). Camden also notes its target demographics are quite suburban in nature (especially in Sun Belt).

13) Like others, Camden reported only minor property damage from recent hurricanes.

14) On the expense side, Camden reported better-than-expected numbers on both property taxes (flat) and property insurance (down 10%, but only after massive hikes in prior years).

15) Like others, Camden said their priority continues to be revenue over rent, and that means reduced rents to keep occupancy high in the face of big supply volumes. Remember vacant unit = $0 revenue.

16) Big picture: The demand story is robust. Supply is the big headwind, but … as I've written about extensively … Camden sees supply peaking and expects rents to rebound as supply drops off.

Centerspace (CSR)

Midwest and Mountain West portfolio with 13,000 units

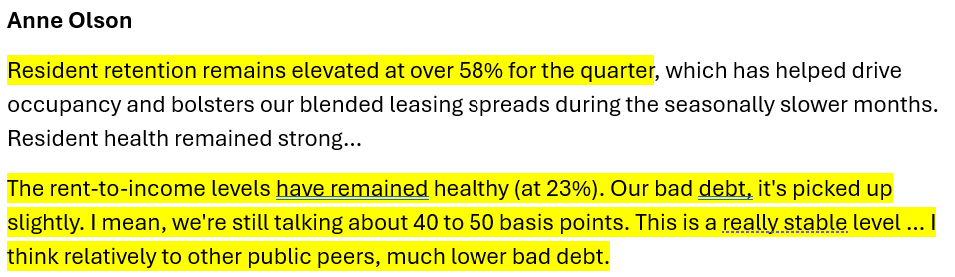

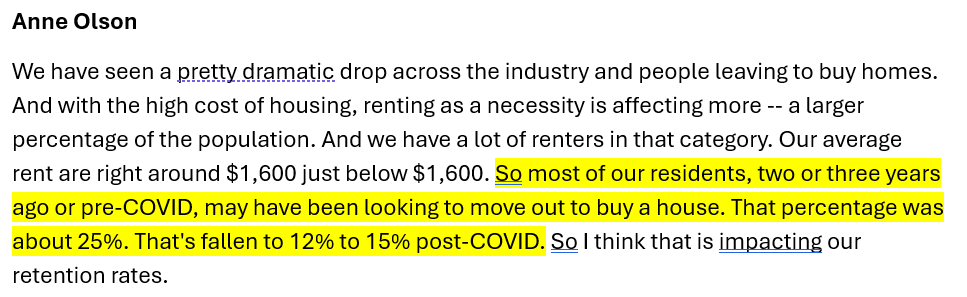

1) Renters remain in financially strong shape. High retention rates, low delinquency and stable rent-to-income ratios.

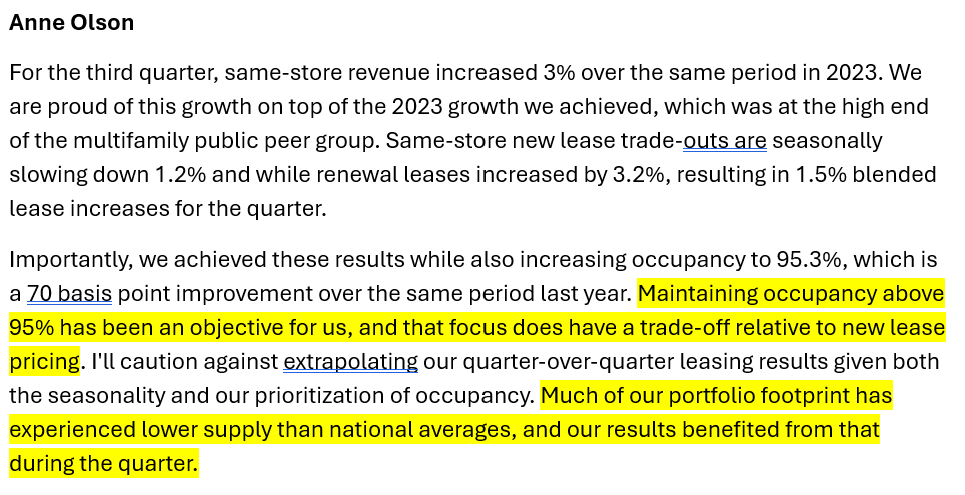

2) Occupancy rates remain very healthy, though Centerspace did report modestly lower-than-expected rent numbers, in part due to continued emphasis on occupancy to drive revenue. New lease rents at -1.2%, renewals at +3.2%.

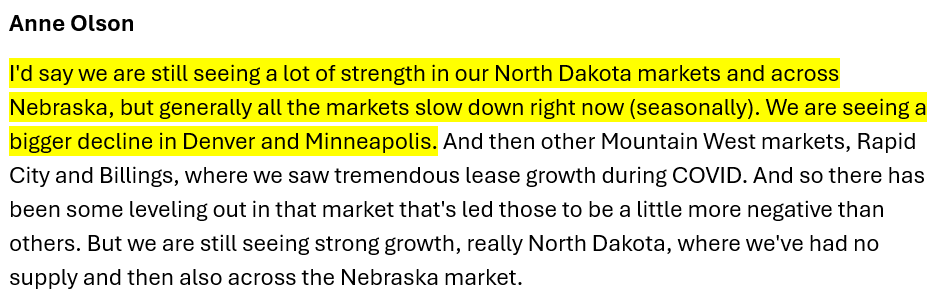

3) There's a correlation between supply and rents. Higher-supplied markets like Minneapolis and Denver are seeing weaker rent growth, while low-supplied markets (including North Dakota and Nebraska) produced higher rent growth.

4) Centerspace partially attributed high retention rates with low move-outs to home purchase -- a common theme across the industry this year (though I don't think it's the only factor in high retention, as I noted earlier in this newsletter with AVB).

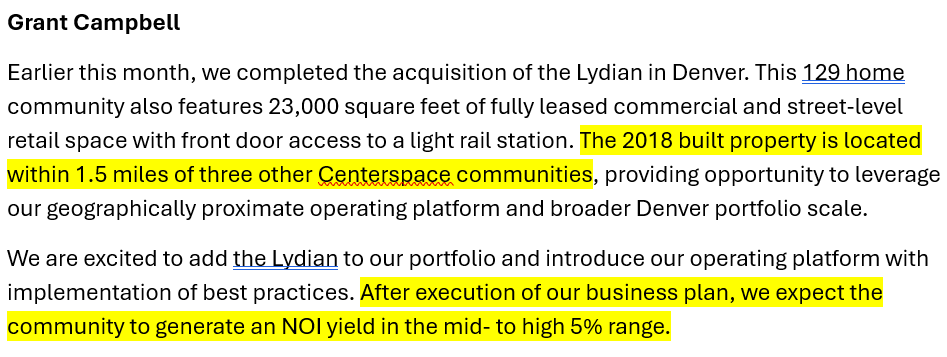

5) Centerspace acquired a 2018-vintage apartment property in Denver. Notably, it's located within 1.5 miles of three other Centerspace properties, which feeds into common strategy these days to cluster properties geographically for more efficient operations / cost sharing.

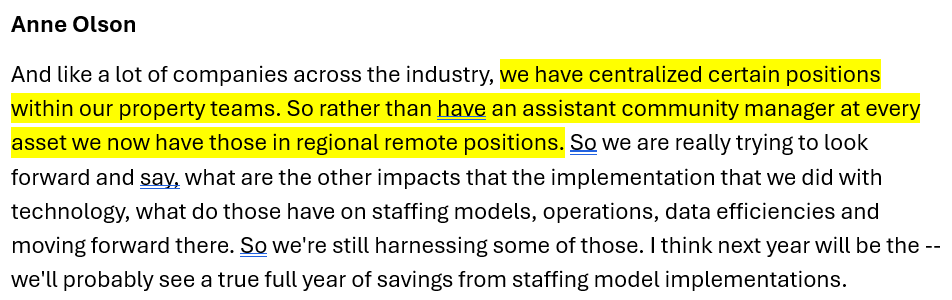

5b) One common way to drive efficiency is to shift the traditional assistant community manager position from an on-site role to a multi-site management role working multiple nearby properties.

Clipper Realty (CLPR)

Portfolio of 10 properties (mostly apartment + some commercial) all in New York City

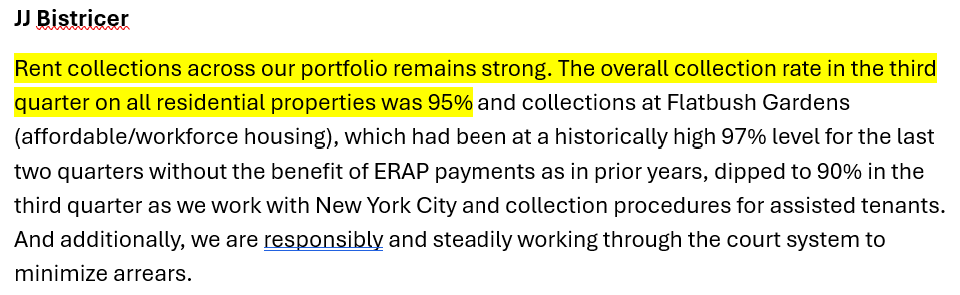

1) There's ample demand and little new supply, resulting in strong rent growth in New York City. That’s a big difference from larger REITs (even the coastals) who see pressures on new lease rents.

2) Rent collections measured 95%, but … were lower in Clipper's massive 2,500-unit affordable/workforce property (Flatbush Gardens) in Brooklyn due to an issue Clipper vaguely referenced as "procedural" and "temporary." And that wasn't the only challenge at Flatbush...

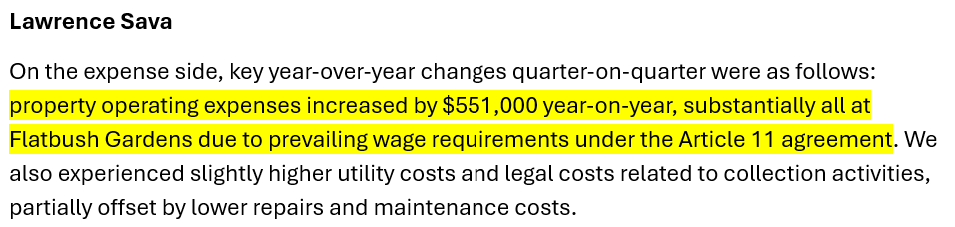

3) Clipper also said a portfolio operating expense hike of $551k was "substantially all" due to "prevailing wage requirements" at the same affordable/workforce apartment property. But on the upside, the property taxes there are now fully abated.

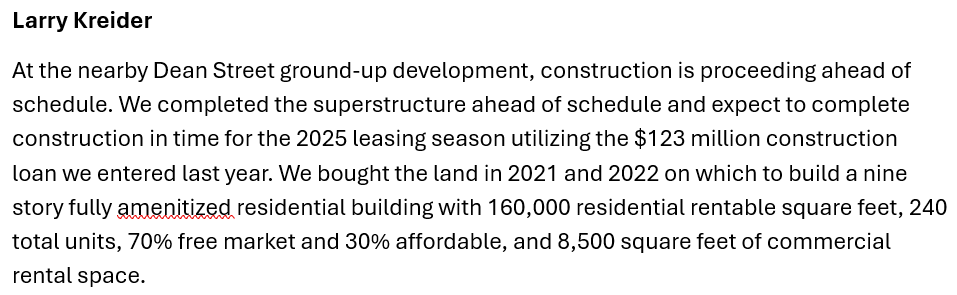

4) Clipper continues to build a new 240-unit apartment property in Brooklyn, which will be 30% affordable units and also include 8,500 square feet of commercial space.

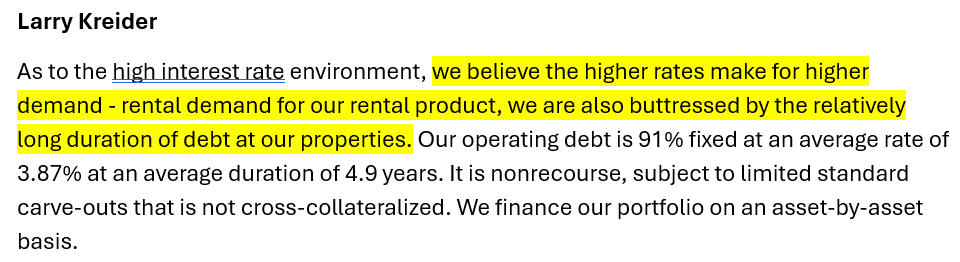

5) Clipper took a pretty bullish stance on the impact of high interest rates, suggesting that'll boost apartment demand. I would think that's less a factor in a market chronically starved of housing supply, but certainly not a negative to apartment demand.

Elme Communities (ELME)

DC and Atlanta portfolio with 9,400 units

1) It's truly a tale of two markets for a REIT that operates in only two markets. DC is strong, while Atlanta is pulled down by high supply + lingering bad debt stemming from COVID-era leasing fraud.

2) First, though, on the macro environment: Elme is seeing a ton of apartment demand, best since 2021. That's driving growth in DC, but even robust demand isn't keeping pace with high supply in Atlanta (which is theme for others operating in ATL, too).

3) Overall, that translates to rent cuts for new leases. But Elme (like others) is still seeing very strong retention rates, boosting renewal rent growth. Occupancy also much higher in DC than ATL.

4) Beyond supply pressures, the other challenge in Atlanta (not just for Elme) has been lingering leasing fraud that accelerated during COVID and has taken a long time to resolve due to slow judicial process. While new tech is helping reduce new fraud, a slow judicial process means it's taken a long time to solve the problem. It's improving due to new state law allowing operators to hire off-duty officers to help with evictions, but slower than Elme expected.

5) In the short term, managing evictions means lower occupancy (low 90s) + higher costs (legal, cleanup, turn, etc). And more vacancy = bigger new lease rent cuts, which Elme estimated at 8-12% for 2024. Longer term, it positions Elme for a rebound in ATL, especially as supply moderates too.

6) Like others, Elme wants to be a buyer in the Sun Belt -- and said they'd soon share investment strategy into new markets. But also noted that pricing is getting "aggressive" as buyers accept Year 1 softness to pursue the buy-below-replacement-cost strategy.

7) Additionally, Elme reported average ROI of 17% on renovation strategies, while also finding NOI improvement through ancillary services like smart home tech + staffing centralization. Also (like others) plans to roll out managed wifi services next year for additional lift.

Equity Residential (EQR)

National portfolio, mostly coastal, with 78k units.

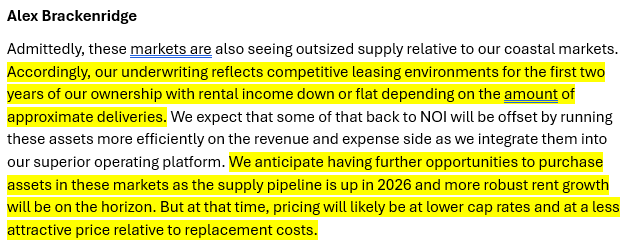

1) EQR says its portfolio is now 10% Sun Belt + Denver, and aiming to be 20-25% "over the next 18-24 months." They're coming in expecting supply-driven softness for 1-2 years because they believe in longer-term upside; and by time supply wanes, pricing would be less favorable.

2) What's driving the shift? EQR shared three factors: First: Diversification. Coastal markets are outperforming now, but they see Sun Belt/Denver as future "revenue growth engine" as supply drops off. (Worth noting Sun Belt outperformed for a ~decade up until supply wave hit.)

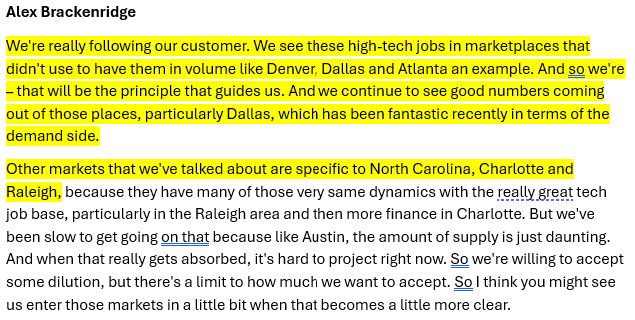

3) Second factor driving the shift: “We’re Following Our Customer.” EQR says its target demographic of higher-income young adults are moving into cities like Denver, Dallas, Atlanta, Austin and (potentially) Charlotte and Raleigh.

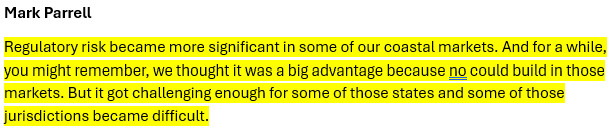

4) Third factor driving the shift: Heightened regulatory risk in some coastal cities. EQR was quite candid about how regulatory barriers have evolved from a positive (big firms like EQR could afford the cost/time to build) to a negative. The “how so? went unspoken, but likely referencing regulatory reach into operations.

And by the way: That's a worrisome reminder that for cities serious about building more housing: It's important to consider lifespan of the 8-9 figure investment, not just the initial construction.

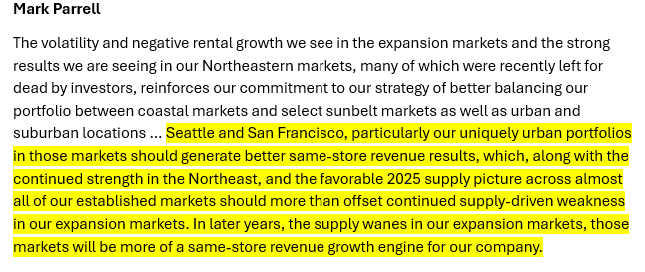

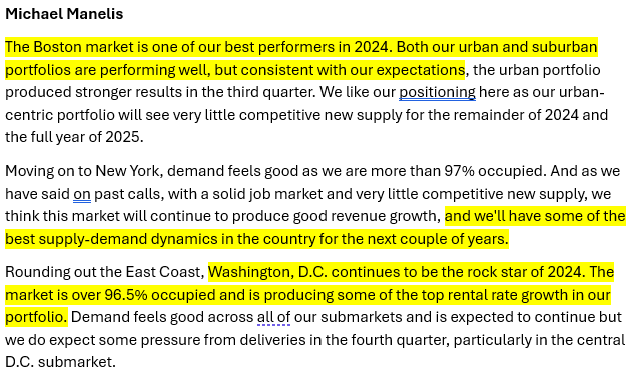

5) On the East Coast, EQR called DC its "rock star of 2024." Boston "is one of our best performers." And New York (thanks to lack of supply) has "some of the best supply-demand dynamics in the country for the next couple of years."

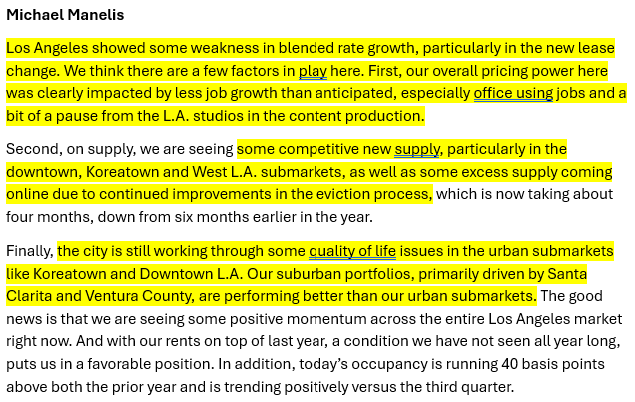

6) Los Angels continues to be a laggard due to lots of Class A supply in the upper-tier submarkets + weaker demand drivers due to soft job market and "quality of life" issues.

7) On the flip side, EQR reported an improving story in San Francisco and Seattle headlined by big employers bringing employees back into the office. In San Francisco, EQR saw 90 bps improvement in occupancy, and partially credited Salesforce.

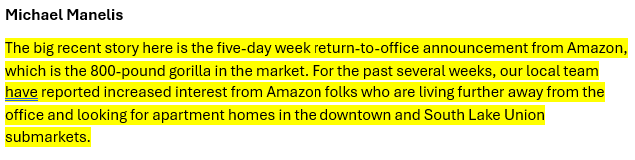

8) In Seattle, EQR reported occupancy above 96% (though with negative new lease rents) thanks to "better than we thought" demand drivers headlined by Amazon's return-to-the-office policy -- directly boosting leasing demand.

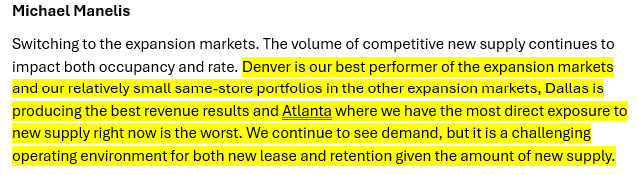

9) As noted earlier, slower going in Sun Belt due to new lease-up competition -- especially in Atlanta, which EQR said has "the most direct exposure to supply right now."

10) EQR (as others did prior quarter) said it remains focused on occupancy -- giving on rent to get higher occupancy = more revenue growth, “which is our ultimate goal.”

11) Continuing an industry-wide theme from throughout 2024, EQR reported continued moderation in expense growth. EQR credited new innovation + cost control measures.

***Now Spinning on the Podcast***

We launched a podcast! Find us on YouTube, Spotify, Apple and Amazon. The Rent Roll with Jay Parsons.

Episode 1: The Case for Middle-Income Housing with special guest Bob Simpson, head of the Multifamily Impact Council

Episode 2: Debunking a Few Multifamily Myths with BSR REIT CEO Dan Oberste

Episode 3: The Hurdles for Apartment Builders with Payton Mayes, CEO of JPI

Episode 4: Fresh Data and REITs’ Earnings Previews with REIT researcher David Auerbach.

Episode 5: Win/Wins for Cities and Developers with Bellevue Mayor Dr. Lynne Robinson

Episode 6: The Politicalization of Rental Housing with ex-Fannie Mae CEO Hugh Frater

Episode 7: Rental Housing 2024 Voters’ Guide with ex-Freddie Mac CEO David Brickman

Episode 8: The Case for New Apartment Construction with Thompson Thrift CEO Paul Thrift

***Episode 9: SFR REITs’ Q3 Earnings Recaps & Outlook with Invitation Homes CEO Dallas Tanner*** (Released yesterday!)

***Coming next week: Episode 10: Apartment REITs’ Q3 Earnings Recaps & Outlook with ex-CEO of Centerspace REIT, Mark Decker*** (Releasing Thursday, Nov. 21)

More on REIT Earnings Season:

If you missed the breakdown of SFR REITs, you can find that here. And stay tuned for an upcoming editions looking at highlights from the remaining apartment REITs: Essex, IRT, MAA, NexPointe, UDR and Veris.

As a reminder once again: None of what I write about REITs (or otherwise) is intended to be investment advice whatsoever, nor is it a comprehensive look at any REIT. I just write about the things I find interesting.

Thank you to the sponsor of this newsletter, Madera Residential. Click the image above to learn more about Madera’s multifamily platform.